- RollUpEurope

- Posts

- Get there before the Patagonia Bros: 3 rollup verticals where multiples are still low

Get there before the Patagonia Bros: 3 rollup verticals where multiples are still low

Have you thought of building starter rollups for Private Equity?

Alex Prokofjev

January 20, 2025

Disclaimer: Unless noted otherwise, views and analysis expressed here are the author's own and based on public sources. The article is intended for informational and entertainment purposes only. This is not financial advice. Please consult a professional for investment decisions.

*********************

Distrust the headlines. Europe is not a graveyard for entrepreneurial ambition. For the risk takers among us, the mass retirement of SME founders presents a once-in-a-lifetime opportunity to get rich while doing something fun. Like rollups.

In Germany alone, 125,000 business owners seek handover every year (source). That’s 342 businesses EVERY SINGLE DAY. Business Services entrepreneurs are particularly exposed due to the intangible nature of the business model and the dependence on the founder.

And who are they going to sell to?

Probably you, my readers. Their kids don’t care. Too small for Private Equity.

What these businesses may lack in size - most are sub 1 million in turnover - they more than make up in affordability. In all but the hottest business services verticals (e.g. MSPs, accountancies) you can roll up individual assets for 2x to 4x EBITDA. Equity is optional with vendor financing becoming mainstream and banks keen to underwrite sticky cash flows.

Buy enough of those, and you can flip to Private Equity for a healthy profit. While this is not the strategy I am pursuing with Baltic Family Capital - we are a forever owner - we have closely studied PE rollup playbooks.

In this article, I share 2 core insights to help you get on YOUR OWN rollup journey:

How to find capital for the smallest of rollups

3 business services verticals ripe for rollup action

Before we dive in: hear it from the M&A practitioners who participated in our inaugural Business Services Summit in London on 26 February 2025:

Outside of PE, is there institutional capital for the smallest of rollups?

YES! The scene is rapidly evolving. Chapters Group was a trailblazer having backed rollups in software, fibre internet and business services (check our writeup). While Chapters has since pulled back from non-VMS verticals, in the last 2-3 years multiple new capital providers have emerged. Like Otium Capital, the family office of the French billionaire Pierre-Edouard Sterin.

Otium likes rollups so much it put out a whitepaper on the topic. It is actually a good read, but if you are in rush, here are the highlights:

Otium seeks to consolidate industries characterised by a) high degree of fragmentation (typical target having €0.5-3M EBITDA) but b) strong growth potential and c) resilience

With a bit of help from leverage, organic growth, and multiple arbitrage investment returns could be as high as 7x over a 5-year period

It’s not all talk. Otium’s biggest rollup so far, a French operator of leisure centres called Hadrena, was projected to hit €200M in revenue and €50M in EBITDA

Inside a Hadrena operated leisure centre (a computer generated image)

Otium competes for talent with LV8, an accelerator-like programme run by the Belgian private equity firm Strada Partners, as well as with search funds (whose numbers have surged, encouraged by successful deals like Water Direct in the UK (article) and Ariol in Spain (article)).

The terms on offer are broadly similar. You get capital to play with, a decent salary - and if things work out, a healthy cut of the exit proceeds. 20% to 30% above a preferred return threshold.

Before you sign up with anyone though… I urge you to consider self-funding. Rob Hill-Smith, the founder of the British HoldCo Perrin & Partners mortgaged his house to get going (check out his thesis here). This sure impressed his other investors. Don’t have the cash? Then commit to a couple of years with a reputable middle market PE like Waterland (their Cooper Parry deal, since exited, was a stroke of genius), Triton or Shore Capital (if you are based stateside).

You will graduate with a bit of cash, a lot of skill - and a network you can raise from.

These 3 Business Services verticals are ripe for rollup action

Let’s warm up with Theme 1: installation and route-based services. The options are almost infinite. HVAC. Pool maintenance. Plumbers. Carpenters. Heat pumps. Garage doors.

To start, choose a vertical with an overlay that makes the service non discretionary (businesses are subject to inspections, humans need warm homes etc.). Bonus points for opportunities born out of crises. For example, Germany teetering on the edge of deindustrialisation due to volatile fossil fuel prices? A boon to photovoltaic installation rollups 1komma5 and Enpal!

Enpal sales grew from €18M in 2019 to €905M in 2023 (source). Because flogging solar panels to end customers is expensive, Enpal’s competitor 1komma5 chose a different path: growing by way of buying installation businesses across Germany (also Australia, Denmark, the Netherlands etc.).

Source: 1komma5

As this Sifted article explains, the Germans’ early success prompted a flurry of new entrants, such as Aira in Sweden; and Hometree and Upvolt in the UK. Their playbooks are fairly similar. It always starts with a consumer keen to reduce energy costs by switching to renewables. A key obstacle is the attitudes of incumbent solar panel / boiler / heat pump installers. Aggregators step in, take over client books - and radically transform customer experience.

Here is what happens next:

Increase installation capacity by recruiting vastly more fitters (according to Manager Magazin, Enpal brings in fitters from Vietnam, Colombia and Bosnia)

Set up a customer portal to book repairs, schedule callouts and buy ancillary services. Drive upsell and recurring revenue

Insource hardware production

Introduce energy management software

Offer finance products like breakdown insurance, 0% downpayment purchase financing etc.

Want to know more? Check out our deep dive on 1komma5°!

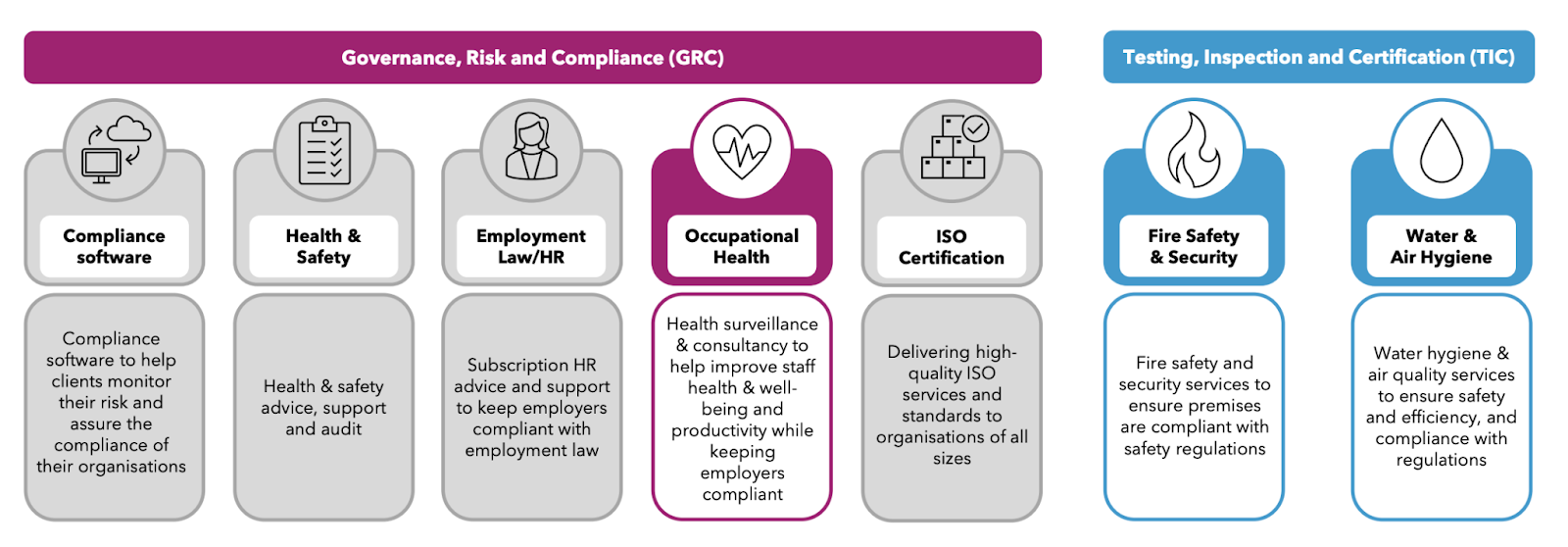

Theme 2 is Governance, Risk, and Compliance, or GRC.

Arsipa achieved a €130M exit to Warburg Pincus 4 years after being founded. Their business model? Buying tiny German occupational medicine and work safety practitioners desperately seeking retirement. Our sources suggest that Arsipa’s buy-in EBITDA multiples of 2-4x compare favorably to the 13x that Warburg paid (heavily pro forma’d at that).

But be careful: focus is paramount. The listed British GRC and Testing “supermarket” Marlowe got carved up by Private Equity after spreading itself too thin.

Source: Marlowe plc investor relations

From what we know, Marlowe’s diversification was forced. It started out as a UK focused fire safety rollup. Then, competition drove up sector M&A multiples (check out our 2-part deep dive on fire safety 🧯 here and here). Marlowe's response was to keep buying, but in less competitive sectors like Employment Law, compliance software, and ISO certification.

The problem with this business model? It wasn’t sustainable.

On the surface, things looked fine. Adjusted EBITDA, Marlowe’s preferred profit metric, kept reaching new heights. Its cash flow statement told a different story: a serial acquirer almost wholly dependent on external financing to keep buying. In FY 2022, Marlowe reported +£9M in operating cash flow and -£324M in investing cash flow. The funding gap was plugged by new debt and new equity.

Eventually, the investors figured it out. The stock plummeted and Marlowe was sold off in pieces.

Source: Marlowe plc investor relations

And finally, Theme 3: digitising (un-)professional services. Recruiters, tax advisors, accountants, estate agents.

I will give you 2 examples from the RollUpEurope community:

Dwelly is rolling up British estate agencies and later rewiring their tech stacks to meaningfully increase profitability

Numeris is rolling up French accounting practices, following in the footsteps of the Aussie aggregator Kelly Partners Group, or KPG.

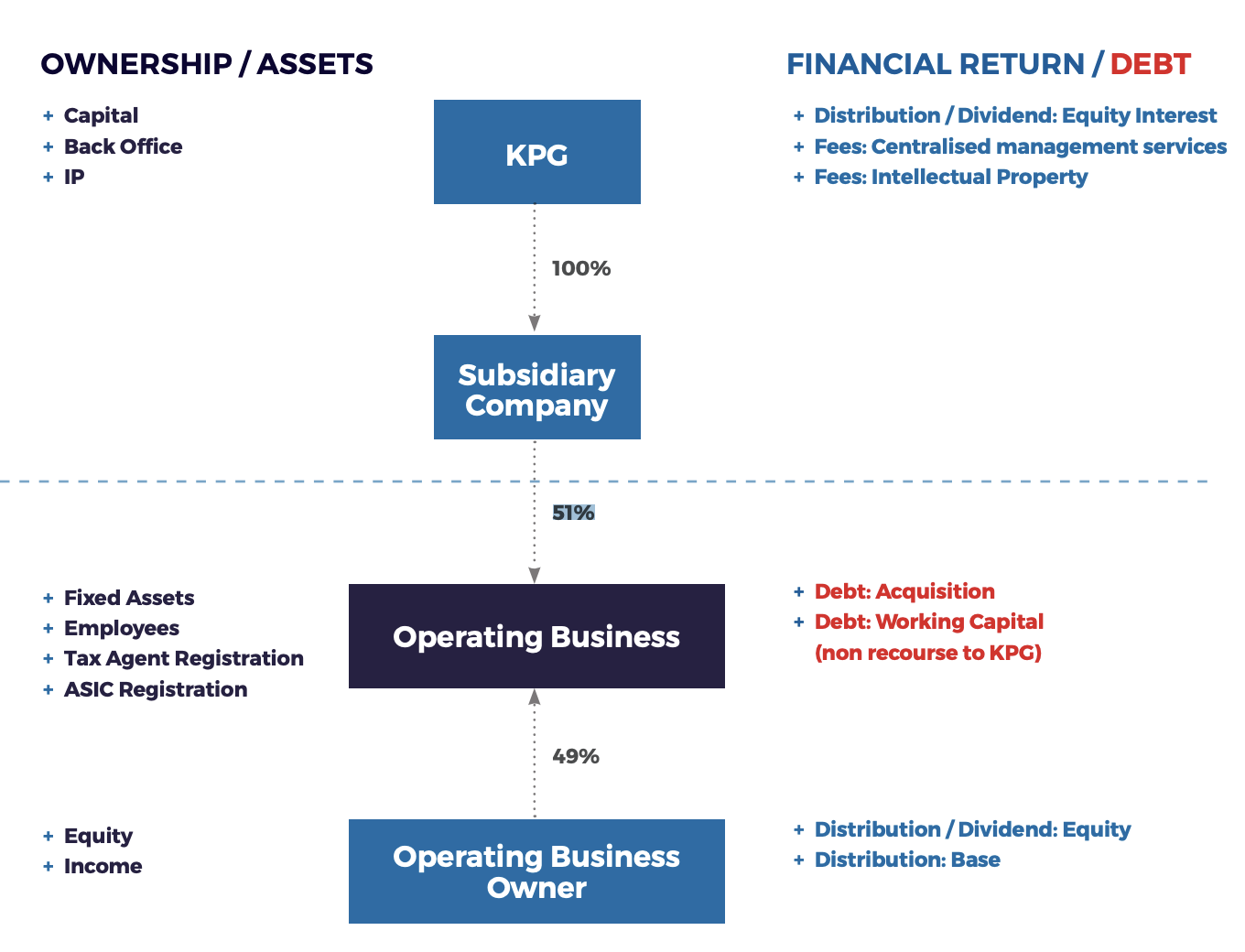

What’s so special about KPG?

Established in 2006 by Brett Kelly, KPG financed the first 14 acquisitions with bank debt - no outside equity - after which it went public. Kelly’s M&A blueprint goes like this:

Always acquire 51%. That way, owner operators are incentivised to remain involved at least for the 10-year initial partnership term

Monthly distributions to partners

Acquisition debt secured against individual operating businesses - no recourse to the TopCo

Provide centralised brand, marketing and systems

10 years ago, KPG revenues were A$20M. Today, well over A$100M.

If Brett can do it, you can do it.

Source: Kelly Partners Group