- RollUpEurope

- Posts

- Are photovoltaic / heat pump installation rollups like 1komma5° worth the crazy valuations placed on them?

Are photovoltaic / heat pump installation rollups like 1komma5° worth the crazy valuations placed on them?

Alex Prokofjev

February 20, 2025

Disclaimer: Unless noted otherwise, views and analysis expressed here are the author's own and based on public sources. The article is intended for informational and entertainment purposes only. This is not financial advice. Please consult a professional for investment decisions.

*********************

For the last two weeks, every morning at 7:45am sharp our apartment building starts shaking as the whirring sound of a boring machine permeates the air. The family on the ground floor who work night shifts at a hospital are decidedly not loving it. The rest of us can’t wait to go carbon neutral.

And, apparently, this is happening all across Europe. For a glimpse of the future, look to Germany where, between 2020 and 2024, installed photovoltaic (PV) capacity nearly doubled, from 54 GW to 100 GW. To put this into context, Germany has about half of America’s PV capacity (source) sitting on less than 1/20th of the landmass.

Germany’s largest solar park, Weesow-Willmersdorf. Credit: EnBW / Paul Langrock

Even more striking are the bottom-up drivers of this buildout. Several million rooftop units went up as consumers and businesses lapped up the subsidies. Alas, in 2024 residential demand for solar plunged as higher interest rates and lower fossil fuel costs took their toll.

Think the industry’s volatile fortunes would scare off institutional investors? Decidedly not. Flush with cash, across Europe, rollups are swooping in on independent PV and heat pump installers.

How sustainable are these aggregators’ business models in the absence of hype money, the flush subsidies - or reliable finance revenue streams, like insurance (hey there, HomeServe)?

We answer this question by breaking down 1komma5°’s business model. This Hamburg based installation startup achieved unicorn status in June 2023, less than 2 years after being founded. Its reported valuation of €1B+ works out to 20x+ 2023 EBIT.

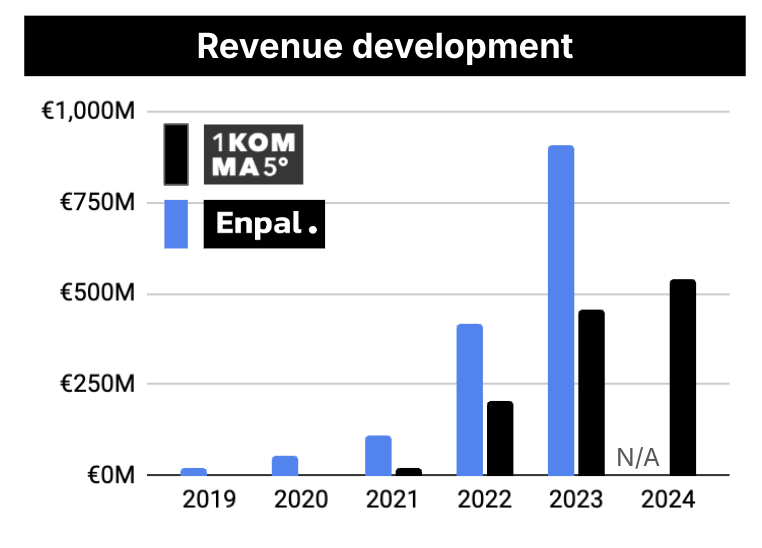

Solar eclipse or not, 1komma5° shows no sign of slowing down. Revenue had surged from 0 in 2020 to €458M in 2023. Last year, revenue grew by 18% to €540M. M&A has been a key enabler. To date, 1komma5°’s has completed 40 acquisitions in Germany, the Netherlands, Sweden, Denmark and Australia. Electricians, heating technicians, solar system builders.

By 2030, 1komma5° aims for revenues of €10B. The investors are happy to underwrite the ambition, judging by the recent €150M raise. An IPO is in the works.

Caption: 1komma5° founder Philipp Schröder

In this article, we break down 1komma5°’s:

Strategy for becoming a giant virtual power utility

Unit economics

Deal structuring playbook

We conclude with an acquisition deep dive on Viasol - a €30M+ revenue Danish PV installer acquired by 1komma5° in 2023. Specifically, we show how 1komma5° took control of a domestic market leader for an estimated 7x EBIT - plus a huge, creative, multi-year earnout.

Two ways to build an installation unicorn, fast

In Germany, 1komma5° is often mentioned in the same breath as Enpal, its older and larger competitor. Over the last couple of years, both companies have delivered stunning revenue growth from a standing start.

Source: company filings, RollupEurope research

Enpal was founded in 2017 by the McKinsey and Rocket Internet alumnus Mario Kohle. At first, it was a pure-play PV installer. Over time, Enpal added energy storage, charging stations for electric vehicles, and heat pumps. By all accounts, it built a formidable sales machine to keep the fitter army busy.

This business model was not without downsides.

The first vulnerability is the tremendous cost of the direct-to-consumer sales effort. According to Manager Magazin, in 2022 Enpal installed 18,000 PVs - a prospect conversion rate of less than 3%. In June 2023, it installed 2,800 PVs. The associated distribution cost was €15M: equating to €5,000 per customer and a whopping 19% of the monthly revenue.

The second vulnerability is the quality issues stemming from skills shortage. Not that Enpal has been standing still. It opened a PV craftsmen academy, pictured below. It has been bringing in fitters from Vietnam, Colombia, and Bosnia.

Enpal PV fitter academy. Source: PV Magazine

Philipp Schröder, the founder of 1komma5° (and the former Head of Germany for Tesla), seemingly sidestepped these challenges by choosing to acquire existing installation businesses. In January 2024, 1komma5° forecast that its revenues would grow from €458M to €750M. Half of the projected topline growth - €140M in total - was supposed to come from 11 acquisitions, all in Germany (source).

PV installation margins are wafer-thin. How does 1komma5° avoid getting burnt in M&A?

As we saw with fire safety rollups, density and route optimisation are key drivers of profitability. 1komma5°’s M&A playbook hinges on finding regional platforms that can rapidly scale both organically and through bolt-ons.

Let’s look at Bode & Stephan, a NW German solar installer acquired by 1komma5° in 2021. According to this article, in the 3 years following the acquisition, the business grew from 1 location to 3, and from 35 employees to 120. Marketing, sales, and accounting functions shifted to the HQ, freeing up operational capacity. The business was promptly rebranded to 1komma5° Gottingen.

Bode & Stephan team. Source: https://www.karriere-suedniedersachsen.de/bode-stephan

As befits a VC backed rollup, buying up humble fitters is just a means to an end. 1komma5° aspires to own the entire value chain. It has talked about insourcing solar panel manufacturing. A proprietary energy storage system is about to hit the market. Finally, there is Heartbeat AI, the software and hardware solution that allows their customers to trade in excess energy.

Software subscriptions and energy trading commissions would fatten 1komma5°’s otherwise wafer-thin operating margins of mid to high single digits. There is not much earnings accretion coming from the near-term M&A pipeline. The 11 targets earmarked for 2024 had an average pre-tax margin of 7%. This works out to an average profit of €1M per target (source).

Source: Manager Magazin, Business Insider, RollUpEurope estimates. 2024 EBIT refers to Operating / Hardware EBITDA

Time will show whether 1komma5° can deliver on the vision of becoming a virtual, decentralized power utility composed of millions of customers using its hardware and software to generate, store, and trade energy.

But even if it doesn’t…it will probably do fine. The group is profitable. It carries no financial debt. It may have missed the 2024 targets by a country mile, but its backlog is solid. And, as you will see in a minute, it has figured out a way to buy prized installation assets for not a lot of money down.

What can we learn from 1komma5°’s Danish purchase?

1komma5°’s, M&A structuring playbook goes like this: