- RollUpEurope

- Posts

- In a world on fire, are fire safety rollups easy money?

In a world on fire, are fire safety rollups easy money?

Alex Prokofjev

January 23, 2025

Disclaimer: Unless noted otherwise, views and analysis expressed here are the author's own and based on public sources. The article is intended for informational and entertainment purposes only. This is not financial advice. Please consult a professional for investment decisions.

*********************

Alright, let’s talk about fire safety: one of 2025’s biggest rollup themes.

Private Equity firms have been gobbling up hardware manufacturers and servicers at a frenzied rate. Last week, a banker told me about a $2M EBITDA German servicer that attracted 20 bids.

What’s not to like?

Fundamentally, fire safety spending is non discretionary. Regulatory requirements around the world are tightening. The investment bank Lincoln International attributes the influx of Tier 1 sponsors (Warburg Pincus, ICG, Ardian) into the market to “the growth of EU-wide regulatory standards, which have significantly tightened in the last few years”.

And for a good reason. In the UK, the terrible Grenfell Fire in 2017 prompted a wholesale revision of fire safety regulations. Inspections and retrofits surged to placate the terrified insurers. In the meantime, wildfires have become ubiquitous, increasingly threatening major urban centres like L.A., pictured below.

Source: BBC

But how exactly does one create value in a fire safety buy & build strategy?

Most individual servicers are tiny (<$1M revenue) businesses led by founders who cannot wait to retire. In the words of one aggregator, “not much talent or value in those businesses”:

They run on antiquated tech stacks

Their topline is skewed towards recurring revenue but no obvious ways to grow installed customer bases, and disproportionate overheads

They operate with suboptimal density and service routes.

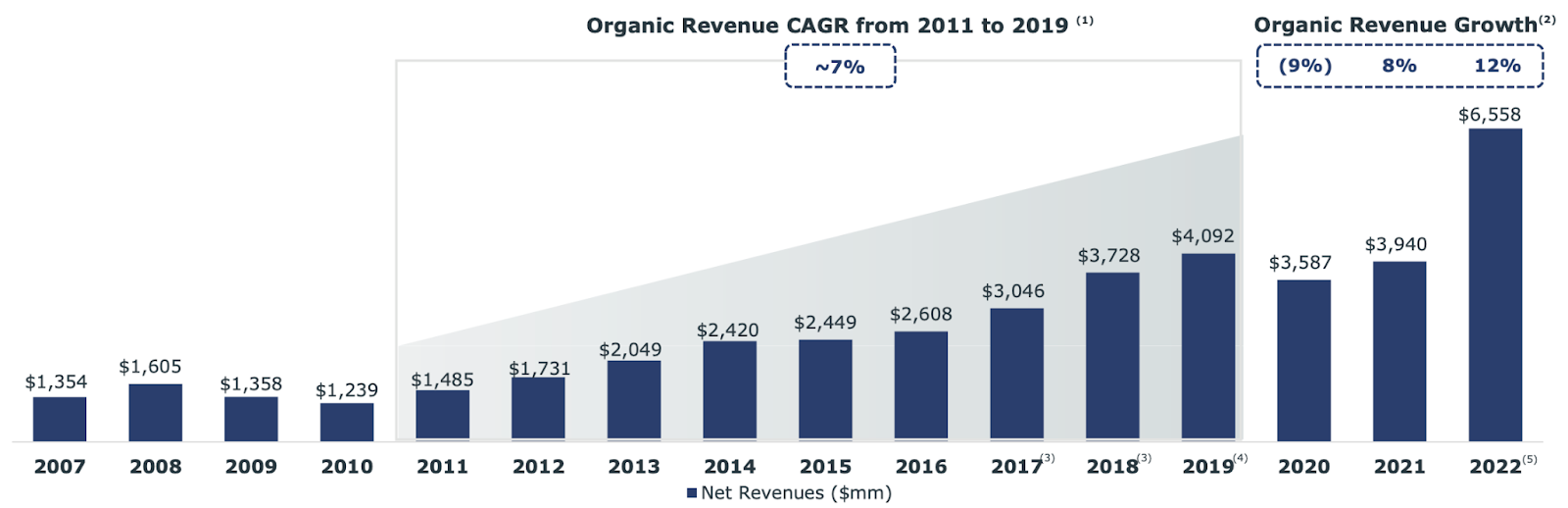

The fire safety game is not for the quitters. You ought to be a glass half full type of person to power through the imperfections of these sleepy yet stable businesses. Rewards can be enormous. APi Group is a $10B market cap aggregator of safety services. Last year, it was expected to deliver $7B in revenue: a 5x increase over 15 years (source).

Source: APi Group

In this article, we explain:

What aggregators see when they see standalone fire safety and security services businesses

How much aggregators pay for bolt-ons

Three steps to drive rollup value post-closing

Reasons why some fire safety aggregators fail

Luis Reyes, a Partner at the Spanish PE firm Iberian Ventures contributed to the article. Iberian Ventures owns Grupo Fire, Spain’s leading fire safety consolidator: 3 years, 21 acquisitions, €8M EBITDA.

Luis Reyes

In Part II of our fire safety series we present a deep dive on Churches Fire & Security, a nearly $100M revenue aggregator backed by the Private Equity firm Horizon.

We reveal the playbook that Churches used to grow revenues 5-fold in 6 years. No we are not talking generic bullet points found in most industry reports. We went behind the scenes, leveraging real customer reviews.

Now: if after this deluge of information you are still hungry for business services rollup intel, join us in London on 26 February for our next Serial Acquirer Summits. Over the course of an afternoon, connect with elite operators building empires in:

💻 IT Services & MSPs

🛠️ Installation & Technical Services (Fire Safety, Security, HVAC)

👥 Professional Services (Accounting, Recruitment, Consulting)

🎟️ Ready? Then grab a ticket now: https://www.eventbrite.co.uk/e/rollupeurope-presents-serial-acquirers-summit-tickets-1206832982939

Contrary to what you might think, installation revenue is actually highly valuable

Here’s why. The incumbent players obsess over preserving the status quo: maximising recurring maintenance revenue. In doing so, they often neglect new installations, which are a source of incremental maintenance.

As a rule of thumb in fire safety, the ratio of installation to maintenance income is 1:20 at best. An installation job of €100,000 results in an annual maintenance contract of €5,000. Even this estimate is generous, assuming that all inspections / corrective work are performed on time.

How does one get hold of installation jobs? In markets with weak GDP growth / construction activity (= most of Europe), there are two main sources. One is direct sales. Not uncommon for aggregators to employ between 25% and 30% of sales people. Another is insurers acting as “channel partners”, referring final audits and implementation of corrective measures to trusted providers.

Key to a successful fire safety rollup? Integration!

Decentralised HoldCo enthusiasts, don't bother. The fire safety game is all about centralisation, optimisation, and ultimately, pricing power.

Let’s start with a unified tech stack. A common CRM and/or ERP unlocks route optimisation and increased engineer utilisation. Regional offices are nixed. Services like invoicing, route confirmation and collections are centralised.

What happens if you do NOT integrate? Consider the cautionary tale of EA-RS, a British provider of fire safety systems owned by the private equity firm Rockpool:

In the course of 2022-24, the company doubled revenue (from $60M to $110M+) off the back of a rapid-fire M&A strategy (13 deals in 18 months!)

However, since integration was not EA-RS’s forte, all those separate instances of CRM and accounting systems took a toll on opex and working capital. Operating cash flow in 2022: +£10M. Operating cash flow in 2023: -£11M

When the sponsor realised the magnitude of the problem, the incumbent CEO had to go. Ouch!

One solution - but not necessarily one team (Source: https://ea-rsgroup.com/)

The reward for well-run platforms? A monster multiple arbitrage!

Based on statutory accounts, multiples in European fire safety bolt-ons look remarkably consistent, between 5x and 7x EBITDA. The true multiples are much, much lower. Pro forma synergies, aggregators aim to pay between 2x and 4x EBITDA. With a platform in place, for each new acquisition gross margin effectively becomes EBITDA margin.

According to our investment banking sources, scaled-up fire safety platforms ($50M+ EBITDA) change hands for anywhere between 10x and 16x EBITDA, financed with 5+ turns of debt.

My head starts spinning just thinking about these numbers!

But how exactly does one add value - outside of leveraged multiple arbitrage?