- RollUpEurope

- Posts

- Tikedo: the Italian search fund printing labels, deals and serious cash flows

Tikedo: the Italian search fund printing labels, deals and serious cash flows

A searcher buys a €6M revenue business. Unlocks an estimated €20M+ carry in <4 years. Keeps going!

Alex Prokofjev

June 26, 2025

Disclaimer: Unless noted otherwise, views and analysis expressed here are the author's own and based on public sources. The article is intended for informational and entertainment purposes only. This is not financial advice. Please consult a professional for investment decisions.

*********************

Which European country is the most underrated in terms of succession opportunities? Italy, hands down. La bella Italia is home to 200,000+ SMEs (excluding businesses with fewer than 10 employees) - second only to Germany in Europe (source).

Italian companies excel at niche manufacturing. Think industries like packaging; high-end textile machinery; precision mechanics; luxury eyewear components; and food-processing equipment.

Also label printing.

One thing that Italy does not have plenty of is search funds. This is about to change.

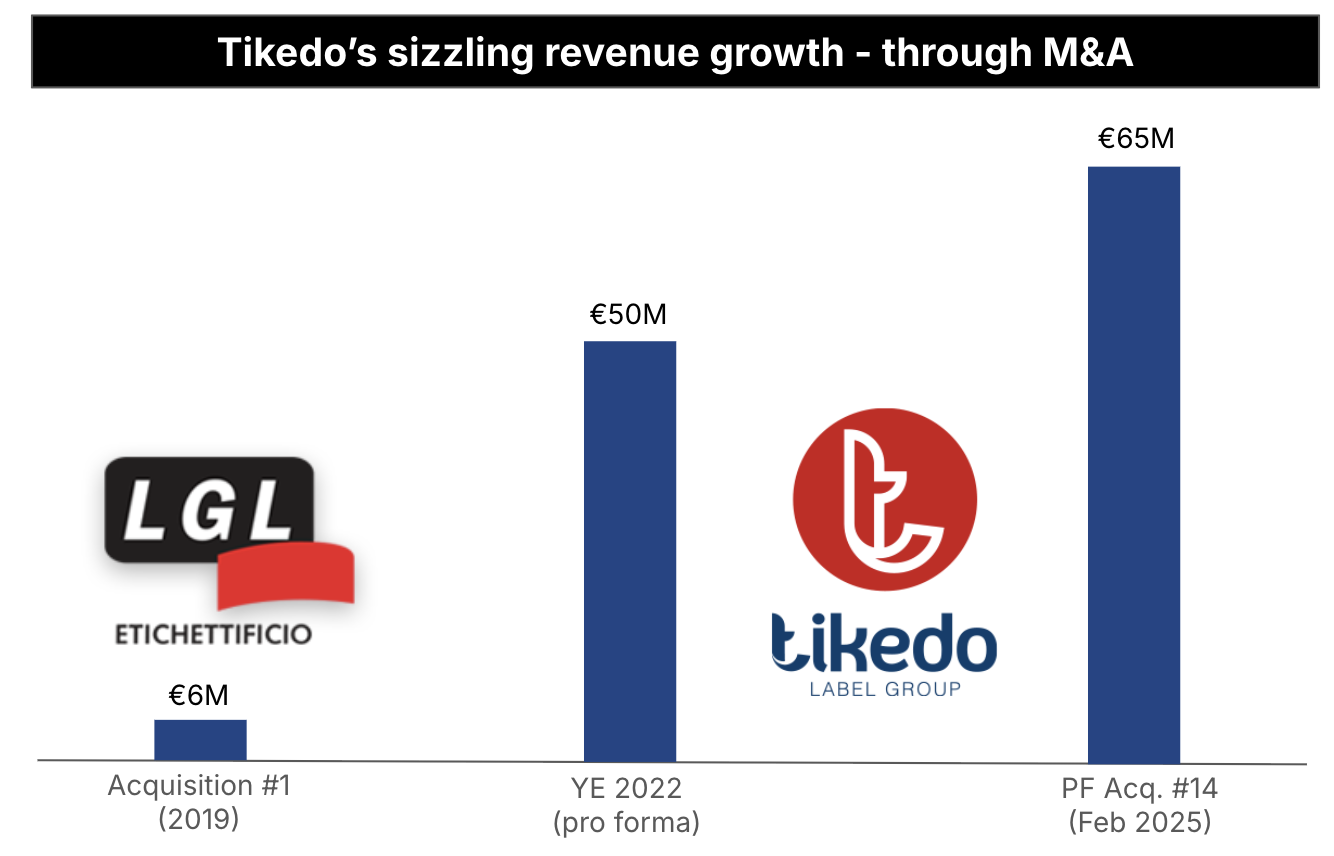

Today, we are bringing you the story of Tikedo: an Italian rollup of label printing companies. With revenues approaching €70M, Tikedo focuses on the Food & Beverage and Home & Personal Care (HPC) end-markets. Tikedo’s portfolio companies excel at manufacturing pressure sensitive labels, sleeves and non-adhesives. Tikedo was majority sold to a Private Equity consortium in 2023, 4 years after Acquisition #1, generating a healthy return for its investors.

Source: BeeBeez, RollUpEurope analysis

We have written about search funds before…

…but Tikedo stands out for two reasons:

Off-the-charts return metrics - we estimate 5x MOIC after only 4 years (vs. average international search fund MOIC of only 2x)

A high intensity buy & build play - 14 deals in 6 years

But first, the backstory.

Tikedo was born out of Maestrale Capital, a search fund founded in 2017 by Vito Giurazza (pictured below left), a onetime investment banker.

A still from a Tikedo promotional video

In 2019, Vito acquired Etichettificio LGL, a Rimini based labelling supplier to the agri-food sector. The target had revenues of €6.4M and EBITDA of €2.4M. 13 more acquisitions followed, mostly of small (€3-5M revenue), niche and profitable businesses.

In 2021, the nascent conglomerate was rebranded Tikedo - a nod to “etichetto”, the Italian word for “label”.

In 2023, a Private Equity consortium acquired 75% of Tikedo, thus unlocking for its early investors an estimated 7x MOIC before searcher carry / 5x post carry. With a chunky rollover, Vito remains at the helm and shows no sign of stopping.

Read on to learn:

Vito’s search fund structure, timeline and return math

Why the label printing industry is primed for a rollup like Tikedo

The playbook that powered Tikedo’s 14-deal M&A streak - including a deep dive on label printing unit economics

Lessons learnt

1. Vito’s search fund structure, timeline and return math

Maestrale Capital launched in February 2017, backed by two dozen Italian and foreign investors. Among Vito’s investors were search fund grandees Will Thorndike, Sandro Mina (founder of Relay Investments) and Jose Cabiedes.

The Etichettificio LGL acquisition was closed in November 2019. End to end, the search took <3 years and cost just under €500K - plus €10M in acquisition equity.

So who ponied up the 10 million? According to public holdings, top 5 investors of the AcquiCo Mistral Holding were:

Vito’s investment vehicle, Vento Holding - 30% (standard searcher carry terms)

Fargo Investments LP - 15%: the investment vehicle of Brad Freeman, a co-founder of the Private Equity firm Freeman Spogli & Co (“Fargo” being the city in North Dakota where he was born)

Relay Investments - 7%: a search fund investor

Branca International - 5%: the Italian spirits conglomerate behind the (in)famous Fernet Branca liqueur

IRS Partners No.22 LP - 5%: aka M2O Inc., the family office of Michael F. O’Connell (whose first investment was National Lines Bureau, a ship mooring company operating at the Los Angeles and Long Beach harbors

Note: for a European searcher to land M2O is a big deal. Michael F. O’Connell and his team have an eye for spotting 10- and 100-baggers. Compounders like the US cold storage giant Lineage - which we profiled here:

Note: our annual subscribers can access Tikedo’s full cap table in the Independent Sponsor Investor Database (free preview below).

No doubt, this is a killer cap table. But don’t feel intimidated.

Vito was 35 when he launched Maestrale. At the time, the median searcher age ex North America was 31 (the metric has been creeping up lately).

Vito did not have prior investing or management experience (he did have an MBA though, from NYU Stern).

In fact, Vito was a mid-level investment banker with JP Morgan.

None of that mattered, because Vito was determined to buy a business.

Looking at Tikedo’s figures today, it is easy to overlook two hard truths.

One, Vito nearly gave up. In 2019, he had a dentistry deal that suddenly collapsed, leaving him exasperated after 2+ years of relentless search.

Two, the Etichettificio deal was a brokered process. So much for proprietary outreach.

In March 2023, Tikedo was sold to an investor consortium led by White Bridge Investments, a Milan based private equity firm. Today, White Bridge and Vito’s search investors that chose to roll over own 75% of the company. Vito retains a c.18% stake. The remaining 7% are owned by 13 individuals - mostly founders of the businesses that Tikedo has acquired.

How much did White Bridge pay for Tikedo? Public filings suggest €74M equity value (for 100%). Adding in the €19M of debt on Tikedo’s balance sheet at end-2022 we arrive at an enterprise value north of €93M, or 9x run-rate EBITDA.

Let me repeat: from €10M to €74M equity value in 3.5 years. A raw MOIC of 7x!

If our calculations are correct, the searcher’s carry back in 2023 was worth €20M+.

2. Why the label printing industry is primed for a rollup like Tikedo

In hindsight, it is obvious that an industry with 1,000+ suppliers (source) that sell into a much smaller number of consumer businesses should consolidate at some point.

A 2022 promotional video sheds light on Vito’s vision:

Step 1: become an Italian market leader - a feat which Tikedo has accomplished, particularly in the food sector

Step 2: build a pan-European player capable of supporting major clients present in Italy, the Iberian Peninsula, France (easily reachable from Spain and Italy), and Germany (a key market for Italian exporters)

There is no forced integration. Tikedo has retained all of the acquired brands, and all the locations

Below is an non-exhaustive list of Tikedo’s acquisitions. It is telling that Tikedo did not venture outside of Italy until 2023, having built up a solid domestic footprint and M&A expertise.

Source: Company disclosure, RollUpEurope analysis

So far so good… but how does Tikedo drive synergies? There are two kinds.

One, Finance and Sales are centralised. The latter is particularly important, giving Tikedo the ability to service major clients across Europe.

Two, by pooling production capacity “the client has the reassurance that they will never experience delays due to, say, a machine stoppage” (source: Tikedo video).

3. The playbook that powered Tikedo’s 14-deal M&A streak

Let’s go back to 2019. Vito bought a business in an industry he had no clue about. What now?