- RollUpEurope

- Posts

- Keeping it cool after 120 deals: Lineage Inc. and the art of cold storage compounding

Keeping it cool after 120 deals: Lineage Inc. and the art of cold storage compounding

2 PE guys, aged 30, buy an old warehouse. End up with a $20B empire.

Alex Prokofjev

February 06, 2025

Disclaimer: Views and analysis expressed here are the author's own (unless expressed otherwise) and based on public sources. The article is intended for informational and entertainment purposes only. This is not financial advice. Please consult a professional for investment decisions.

*********************

It takes some imagination to visualise the mammoth scale of Lineage, the world’s biggest rollup of cold storage facilities. Lineage’s global capacity is 3 billion cubic feet, or 85 million m3. This is equivalent to the combined residential refrigeration capacity of the United States. That’s 130 million households x 20 cubic feet average fridge size (some households have more than one fridge).

Lineage’s warehouse in Chicagoland. Source: company website

We couldn’t help but cover Lineage since it keeps coming up in conversations with the readers. Why is that? We surmise, for two reasons:

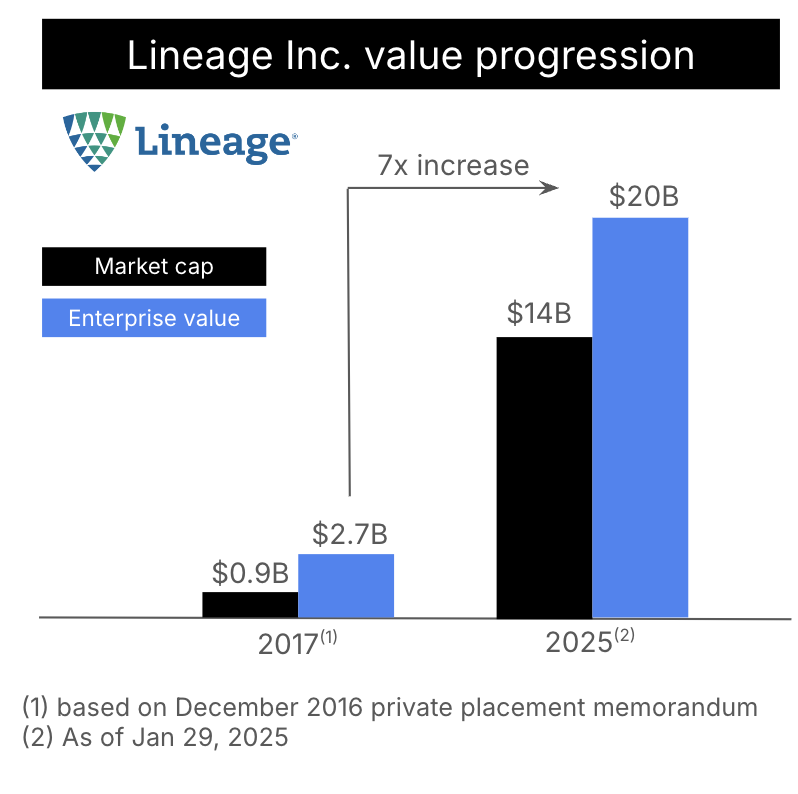

Lineage’s gravity defying growth trajectory: from a single facility in 2008 to nearly 500 today. From 0 to $5B+ in TTM revenue (source). From 0 to $20B enterprise value (source)

30: Adam Forste’s and Kevin Marchetti’s age when they founded the business. Today, Adam and Kevin hold Lineage stock worth a few billion dollars…each

Left to right: Adam Forste and Kevin Marchetti. Credit: CNBC

In this article, we go over:

The investment case for cold storage

How Lineage got going in the aftermath of the 2008 financial crisis

Why private credit has been a key enabler of cold storage rollups

Lineage’s M&A playbook - and why it is relevant for any industry with lots of family owned businesses

Four key lessons learnt

Source: Rollupeurope analysis

The investment case for cold storage…

…is straightforward: humans need food to function. That food needs to be stored somewhere. As populations urbanise, food supply chains become more complex. Moreover, city dwellers consume vast amounts of frozen pizzas and ready meals.

Packaged foods, such as pizza, represent 11% of Lineage’s revenue. Credit: Martin Wombacher

Now, the good news is that the food storage industry has demonstrated resilience through all the recent crises. The consumers are locked in, but so are the food producers and the retailers: facility switching costs are enormous. Customer churn is thus minimal. According to Lineage’s key peer / competitor, Americold, its top 25 customers have been with the firm for an average of 37 years (source). For Lineage itself, the comparable figure is “30+ years” (source).

What else? The proportion of recurring revenue is steadily growing. 40-50%+ of Americold’s and Lineage’s contracts (source) have revenue commitments.

The upshot is a business model that supports mid-20s EBITDA margins with OK macro growth.

At the same time…

Cold storage facilities are both less fungible (from a conversion point of view) and more capital and operationally intensive compared to traditional warehouses. And, unlike in “dry” warehouses, where the ramp-up to target occupancy is relatively short, greenfield cold storage properties take time to turn cash flow positive due to high overheads, especially power and refrigeration.

Thus, entry barriers are HIGH. A typical cold storage warehouse is 20-30 years old, implying that new supply is scarce. It costs 2-4x more to build compared to a traditional “dry” warehouse.

So, why build when you can buy?

Originality is optional: how Kevin and Adam got going

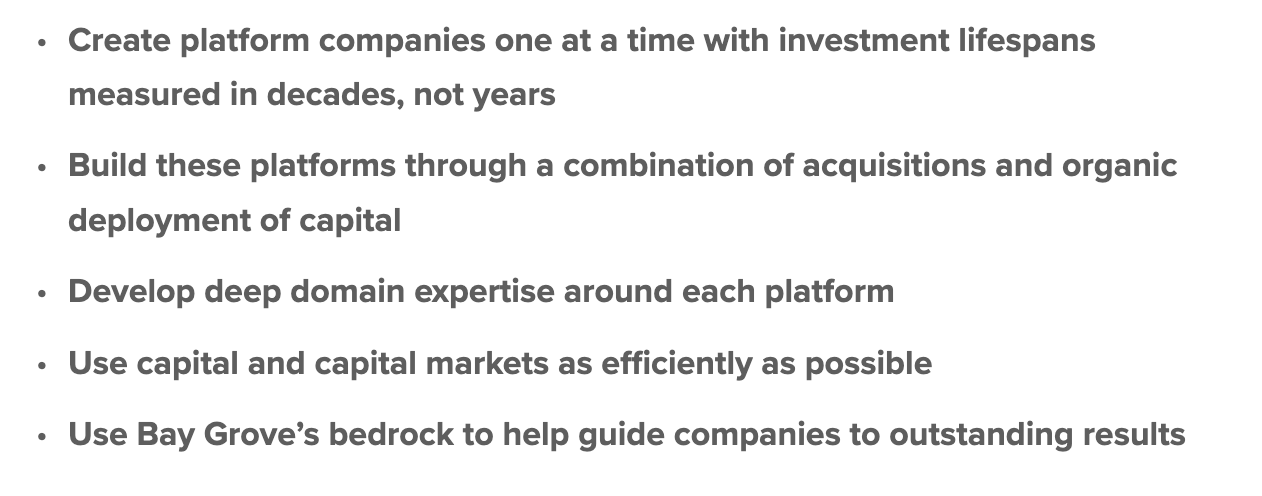

For me, the most striking part about Lineage’s story is the early days. In 2007, Kevin and Adam raised money from 30-odd investors for Bay Grove, an investment company whose objective was to create several “long term platforms” (i.e. rollups).

Bay Grove’s core tenets

Kevin and Adam had met in the Morgan Stanley investment banking analyst programme, after which both switched to the buy-side. Kevin went to Yucaipa Companies and Adam to KKR.

Kevin’s pick proved highly consequential, given Yucaipa’s retail and hospitality investment pedigree. In 2008, Yucaipa acquired Americold, the cold storage market leader at the time. As Kevin admitted in a 2023 interview, being involved in the transaction made him realise that the market could sustain more than one aggregator.

Sidenote: in March 2008 (before Lehman and all!) Americold traded for $1.5B enterprise value. At the time of writing, Americold’s EV was worth $10B (source).

It gets better. Americold’s contribution to its future nemesis was far more than providing inspiration. According to the same interview, the Americold management sourced Lineage’s first deal, too: the Seafreeze facility in Seattle. Apparently Americold was too busy to consummate a $20M acquisition, notwithstanding the $10M haircut on the asking price after the previous bidder had their financing pulled.

Kevin and Adam had 8 weeks to close the deal. In these 8 weeks, they were negotiating with 5 stakeholder groups in parallel (the city, the union, the debt investors, the equity investors, and the port - from which the land was leased).

After the deal closed, the duo spent a year in the Northwest, learning the ropes. A year later, a second Seattle asset was acquired and merged with Seafreeze.

Things were about to get serious - with the help of a new friend.

Private credit funds: rollups’ best friends

Let’s take a step back. Why do standalone cold storage players like Lineage and Americold even exist? Why don't their clients do it themselves?