- RollUpEurope

- Posts

- Landscaping roll-ups: PE's new frontier or a thorny proposition?

Landscaping roll-ups: PE's new frontier or a thorny proposition?

Bonus: Idverde and Green Landscaping Group tear-downs

Pavel Prokofiev

February 25, 2025

Disclaimer: Unless noted otherwise, views and analysis expressed here are the author's own and based on public sources. The article is intended for informational and entertainment purposes only. This is not financial advice. Please consult a professional for investment decisions.

*********************

Imagine: you are a Private Equity professional, tired of chasing the same business services roll-ups as your peers. Vet clinics. Medspas. Fire safety. HVAC. The stuff that seemingly everyone is looking at, and bidding for. Then suddenly, in the distance you spot a lush, green opportunity.

The opportunity is exotic - but who cares when the fundamentals are rock-solid? The business is plentiful and highly recurring. Loyal customers. Gross margins hovering around 50%. Finally, a huge TAM: $153B in the US alone (source) - larger than the HVAC market! (source).

Source: Better Business Bureau, IBIS World Landscaping Services Industry Report

Is this an oasis or a mirage? Welcome to the world of landscaping: a new roll-up frontier! The early settlers seem to be doing alright. Europe’s 3 largest landscaping aggregators - Idverde, The Nurture Group and Green Landscaping Group - sport combined revenues north of $2B.

Source: public filings, RollUpEurope analysis

Read on to learn:

Why major PE firms like KKR are all-in on lawn care

US landscaping economics…

…and why the game is different in Europe

The financials of Green Landscaping Group and Idverde, Europe’s landscaping M&A pioneers

5 ways in which PE firms cultivate returns in the sector

The RollUpEurope verdict: is landscaping the next HVAC?

American PE firms and family offices are piling into landscaping big time…

…We are talking about names like Comvest Private Equity (Bland Landscaping), KKR (Brickman Group), CI Capital Partners (Mariani Landscape), and Signal Hill Equity (Urban Life Solutions).

Why are these heavyweights suddenly interested in lawn care?

The allure lies in a combination of factors:

The “Silver Tsunami”. Let’s zoom out. Across OECD, hundreds of thousands of baby boomer business owners are in - or past retirement age. As is often the case with unglamorous blue collar businesses, the kids aren't interested in taking over

Early mover advantage: In landscaping, the roll-up game is just getting started. Out of an estimated 661,000 landscaping businesses in the US, only a fraction are sponsor-owned

Relative value: For the price of one HVAC business, you could acquire two or three landscaping firms. Single assets change hands for 3-4x EBITDA compared to 11-14x for at-scale PE-backed platforms.

Is there a catch? Oh yes!

The dirt beneath the surface: US landscaping economics

Based on our research, a “typical” target will have:

Revenues of $2.5M to 8M

Gross margins of 50%

EBITDA margins up to 20% ($0.5-1.5M for a “typical” target)

CAPEX consuming 5-6% of revenue

EBITDA-CAPEX around 12% of revenue

To succeed in this game, you will need patience. Since the individual targets are so small, you have to acquire lots of them to achieve a PE-worthy scale. Getting to, say, $15-20M cash EBITDA requires ±20 acquisitions.

Also, though landscaping sounds like easy money, it comes with a raft of operational challenges. We list the top 5 below.

Number one, every property is unique, which means operational complexity. Plot sizes are different. Plant types are different.

Number two, no real economies of scale in this hyper-local industry. Similarly to fire safety rollups (link to our primer), efficiency gains arise from outer density (i.e., minimising drive times and maximising the number of appointments) and labor utilisation.

Number three. Customers stick around - because who likes shopping for a gardener? Having said that, competitive intensity, and therefore margins, vary wildly region by region. Pricing is crucial (to account for inflation etc.) since organic growth is hard to come by in most places. The customers who move across from competitors tend to be price-conscious and as a result, have shorter lifespans than the installed customer base.

Number four - this is a big one - workforce issues. Due to a high percentage of illegal labour, the industry is bracing for the impact from stricter US immigration policies. This comes with wage inflation and loss of know-how and client relationships.

Number five, seasonality - depending on location, of course. There’s nuance. In the Northeast US, snow removal in the winter provides additional revenue. The sunny Florida: offers year-round maintenance opportunities, albeit, with fluctuating margins as hot weather increases the need for watering which in fixed price contracts increases labour costs.

What about Europe?

The European landscaping market differs from the US in two key respects:

Firstly, the public sector (i.e. local authorities) is the main source of business. This is due to the Europeans’ lower purchasing parity; the higher % of population residing in multi-unit dwellings; and of course, the higher tax burden.

Secondly, unlike in the US, there is limited equity capital available for the sector, and few brokers that truly understand it. As for the debt piece, the banks’ relative unfamiliarity with the industry is offset by the revenue visibility associated with public sector contracts.

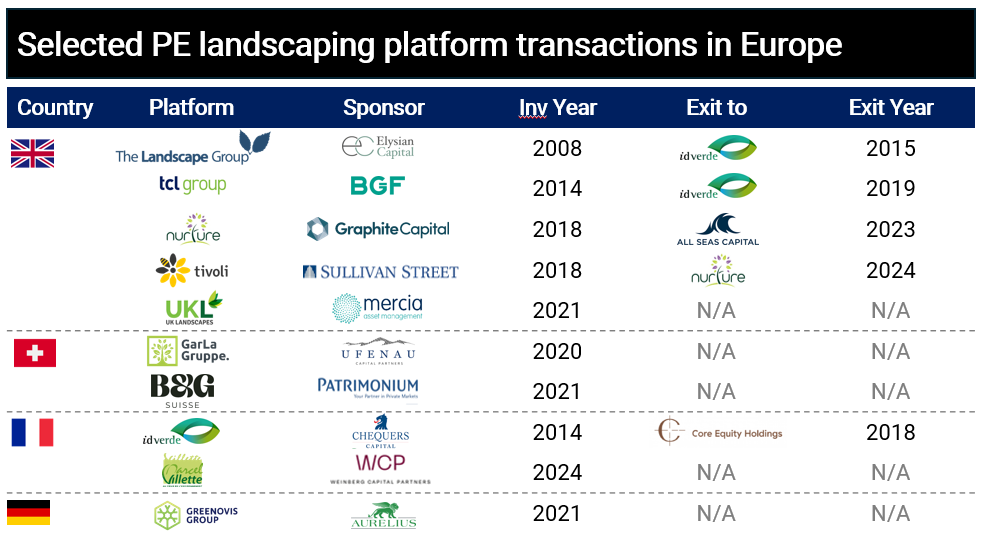

Some of the largest consolidators include Nurture Group in the UK; Idverde in France; and Green Landscaping Group in Sweden. The first two are PE-owned (Allseas Capital and Core Equity); the third one is publicly listed.

Other notable players include GarLa Group (Ufenau), Marcel Villette Group (Weinberg Capital Partners), B+G Suisse (Patrimonium), and Ringbeck (Aurelius Equity Opportunities).

Source: public filings, RollUpEurope analysis

Below, we profile Green Landscaping Group and Idverde.

The Stockholm-based Green Landscaping Group, or GLG, operates in 6 countries including Northern Europe and DACH.

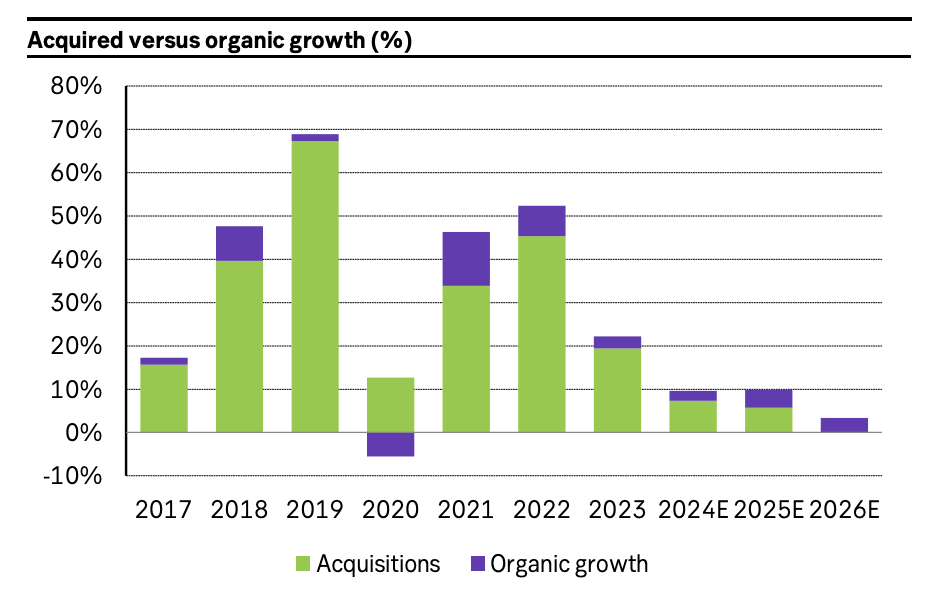

Long-dated public sector contracts represent 2/3 of turnover. GLG’s c.$350M market cap compares against FY24A revenue of $590M and EBIT of $40M (c.7% margin). GLG is pretty good at what it does, as evidenced by the 26% revenue CAGR and 37% EBITDA CAGR over the last 5 years (source: ABG Sundal).

According to the Swedish bank SEB, much of this growth has been M&A driven:

Source: SEB

Since going public in 2018, GLG has completed c.40 acquisitions. That’s 2 to 8 per year, with a median turnover of $5M and 30 employees. Originally a Nordic pure-play, recently GLG has made a big push into German-speaking Europe. GLG pays multiples of 4-6x EBIT according to ABG, which compare favourably to its valuation of 15x FY24A EV/EBIT based on SEB estimates.

Here is a video of the GLG CEO Johan Nordström presenting the equity story.

Notwithstanding this impressive growth, GLG’s share price performance has been lackluster. GLG listed in early 2018 at SEK 21/share. Starting in 2020, share price had run up almost five-fold, after which it has been see-sawing.

Source: Factset

What happened?