- RollUpEurope

- Posts

- Why outsourcing giants are gobbling up ServiceNow partners

Why outsourcing giants are gobbling up ServiceNow partners

How Sunstone Partners made 4x with Thirdera in just 3 years

Alex Prokofjev

June 25, 2024

Who doesn’t like efficiency?

Software giants like SAP, Salesforce and ServiceNow have all anchored their USPs on the promise of faster month-end closings; happier, more productive workforce; reduced ticket backlogs; and more transparent sales pipelines.

Judging by the frenetic activity challengers small and big (recently we wrote about Atlassian, which has set it sights on IT Service Management, ServiceNow’s bread and butter), you would think the incumbents are feeling threatened.

They are not. One big reason is their armies of “partners”: Value Added Resellers and System Integrators. Firms that distribute, implement, customise and maintain software. According to BCG, some clients rank System Integrators more highly than the vendors they represent.

An estimated 70% of SAP S/4HANA deployments are of the “brownfield” kind, meaning, they replace in-house or point solutions. Smooth transition is thus critical. Post implementation, partners act as the “first line of defence” against decommissioning.

There are two main categories of partners:

Embedded within major Global System Integrators (GSIs) like Accenture, Cognizant, IBM, Fujitsu and Infosys

Small, regional players and their consolidators. Think Adaptavist for the Atlassian ecosystem, Thirdera for ServiceNow (now part of Cognizant), OSF Digital for Salesforce etc.

Increasingly, the trend is this. Once a partner ecosystem reaches certain maturity, savvy, well capitalised aggregators emerge. More often than not they are PE backed and laser-focused on exiting to a GSI.

And exit they have.

Scaled up partners, those with $20M+ in revenue and meeting / exceeding Rule 40 on a standalone basis, have sold for 3-4x revenue or 15-25x EBITDA.

Here are just two examples from the ServiceNow ecosystem which we are going to zoom in on for this article. Thirdera was sold for $420M after 3 years, generating a 4x+ return for Sunstone Partners. GlideFast was sold for $350M after 2 years under PE ownership (7 years of operations).

Source: Thirdera

In the next 2-3 years, we are going to see a torrent of exits like these.

In this article, we cover 4 topics:

What is ServiceNow - and why does it need partners?

Trends in ServiceNow partner M&A

Why the M&A game is getting harder (paid subscribers)

Thirdera case study: how Sunstone Partners made a fortune rolling up ServiceNow partners (paid subscribers)

Where next? 5 ecosystems ripe for a partner-led aggregation strategy (paid subscribers)

Wait, that’s not all! While researching for the article we updated our serial acquirer database. The database lists 50+ aggregators of system integrators and MSPs across North America, Europe and Australasia.

Enjoy!

What is ServiceNow - and why does it need partners?

The Santa Clara, California headquartered ServiceNow is a cloud-based workflow automation platform. Its bread and butter are Enterprise Service Management solutions used by very large, complex organisations like JP Morgan, Goldman Sachs or Infosys.

Source: ServiceNow

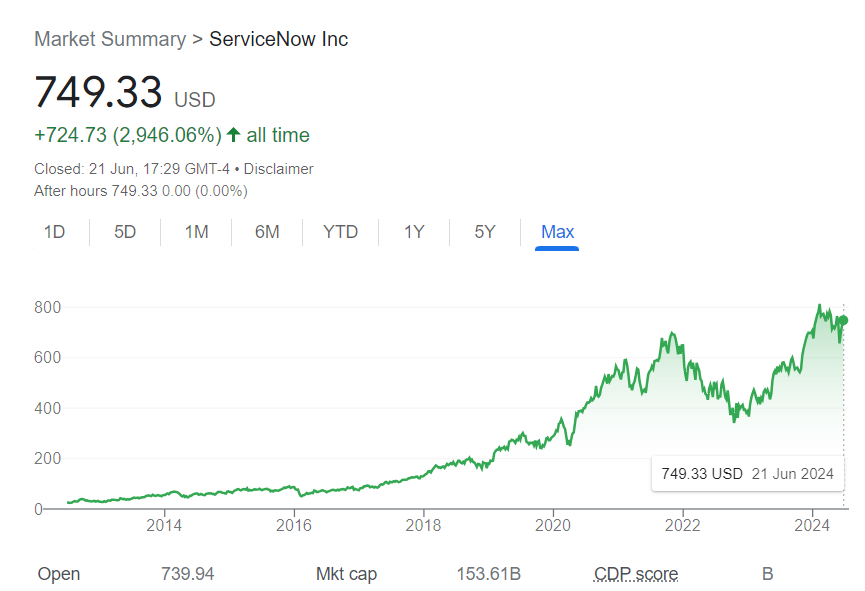

ServiceNow’s $150B+ market cap is a function of its size ($10B+ run-rate revenue), growth (still pumping out 20%+ YoY) and 99% renewal rates (SaaStr did a good refresher on ServiceNow).

All the while delivering free cash flow margins of 30%+.

The upshot? If you had invested in ServiceNow at the 2012 IPO ($18/share), you would be up more than 40-fold by now!

Source: Google Finance. Market data as of COB 21 June 2024

A lot of this growth is due to the substitution effect. Goldman Sachs estimates that in the US alone, on-premise, custom workflow applications represent a $1T market.

ServiceNow’s partner network, now 2,000+ firm strong, has been very effective in delivering on that opportunity while fighting off competition from Workday and Salesforce.

Partners are grouped into 6 tiers based on their expertise and track record, from “Registered” to “Global Elite”. Only 6 firms have made the Global Elite cut: Accenture, Deloitte, DXC, KPMG, EY and IBM. The next tier, Elite, is much larger, with 160+ firms, including Cognizant, Infosys and TCS.

As to why the reasons why ServiceNow would not turn on its partners in pursuit of ESM ascendancy, one management consultant I spoke to reeled off a whole list:

“Retaining ServiceNow valuation requires focus on software, not services (which are lower margin)”

“ServiceNow’s partner network supports its growth ambitions

“ServiceNow CEO Bill McDermott has a history of investing in partners going back to his time at SAP”

And my favourite:

“All of their peers are doing this”.

Trends in ServiceNow partner M&A

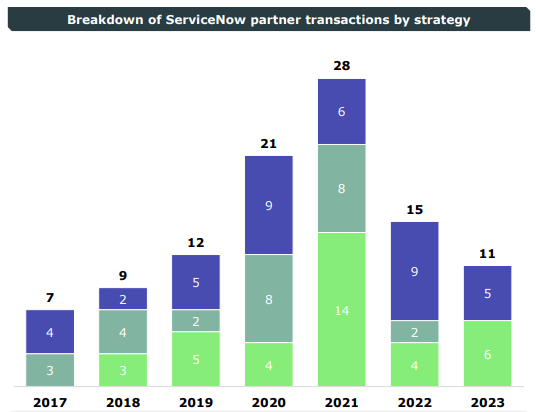

As the chart below shows, since 2017 there have been close to 100 M&A transactions involving ServiceNow partners (access dives here: ChannelE2E, Equiteq, BDO).

Deal flow began to pick up in 2019, when ServiceNow transformed its partner strategy, launching new partner designations and growth-inducing initiatives (e.g. a dedicated business development team).

M&A activity reached frenetic levels in 2021, buoyed by multiple tailwinds (record PE dry powder, Covid induced pickup in demand for digital transformation etc.). In 2022, ASGN paid $350M for GlideFast, a BV Investment Partners owned rollup. GlideFast was on track to generate $95M in sales (growing 30% YoY), with a mid-teens margin. It had 350 consultants.

A nice 3.5x revenue / 25x EBITDA exit!

Source: Equiteq

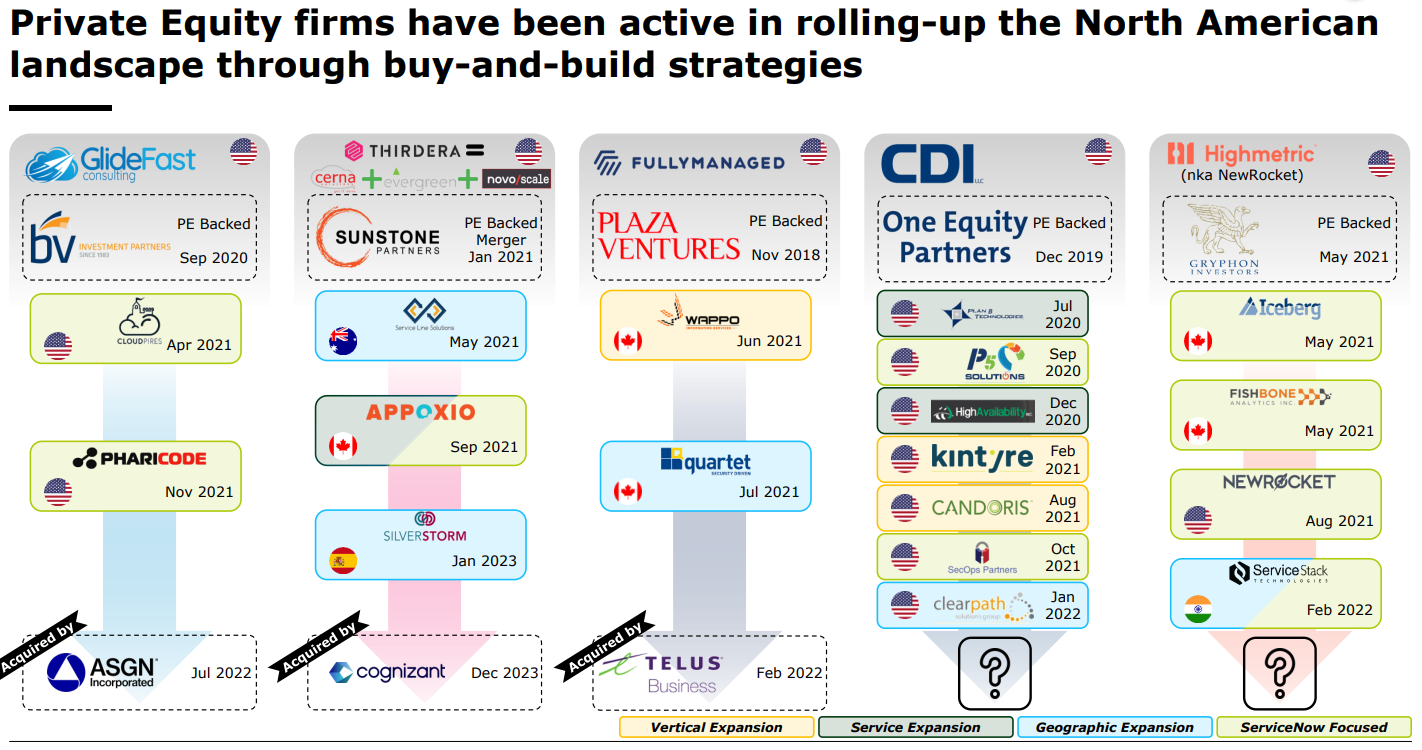

A typical acquisition target is an Elite partner with several hundred consultants, itself a product of M&A, and backed by mid market private equity firms like One Equity Partners, BV Investment Partners, Plaza Ventures and Gryphon:

Source: Equiteq

Most recently, Infocenter was acquired by Insight Enterprises, a Fortune 500 Solutions Integrator, for a rumoured 5x revenue.

Scale is crucial too. According to Michel Regueiro, a consultant to ServiceNow boutiques:

Boutiques with <$10M in revenue see valuations around 1-1.5x revenue, whereas those above $10M can expect 2-2.5x. Firms exceeding $20M might even achieve 3x, with the industry high around 4.5x.

The M&A game is getting harder

There is no shortage of PE money chasing existing and emerging partner rollups. However, a generic consolidation strategy simply does not work anymore. There are three main reasons for this.

One, the growing specialisation among boutiques - endorsed by ServiceNow - requires deep domain expertise while naturally limiting the amount of capital that can be profitably deployed.