- RollUpEurope

- Posts

- $7M to $400M revenue in 10 years, 16 deals & STILL bootstrapped: Adaptavist’s incredible story

$7M to $400M revenue in 10 years, 16 deals & STILL bootstrapped: Adaptavist’s incredible story

THE installation rollup for the digital age

Alex Prokofjev

June 14, 2024

Atlassian, the Aussie collaboration software giant, is riding high. Never mind the share price that lingers two-thirds below the 2021 stratospheric highs.

At $5B ARR, Atlassian is still growing 30% YoY!

Atlassian’s products went mainstream a long time ago. People may b*tch about Confluence, make memes about Jira - but they keep using the tools.

Source: BCG

And though Atlassian prides itself on being “the biggest product-led enterprise software company in the world” (it has 300,000 clients), the reality is more nuanced.

Like its workflow / productivity software brethren Salesforce, Monday and ServiceNow, Atlassian relies on 900+ partners to peddle, tailor, install and maintain its products.

50% of Atlassian’s revenue is transacted by partners vs. 10% a decade ago. Partners are essential to Atlassian’s strategy of taking a bite out of ServiceNow’s lucrative ITSM franchise. As the Atlassian CRO Cameron Deatsch commented, “we never want to give our customer any reason to not work with a partner”.

These partners and help keep Atlassian’s sales & marketing costs low. In fact, very low compared to the peers:

Source: Atlassian FY24 Investor Day

How is this possible?

The bulk of Atlassian’s revenue comes from enterprise clients: corporations that bring in $10,000+ in annual revenue. For them, Jira adoption is part of a broader digital transformation agenda, moving workflows to the cloud. They need hand-holding. Furthermore, Atlassian’s decision to sunset server product in 2024 turbocharged demand for cloud migrations from existing clients.

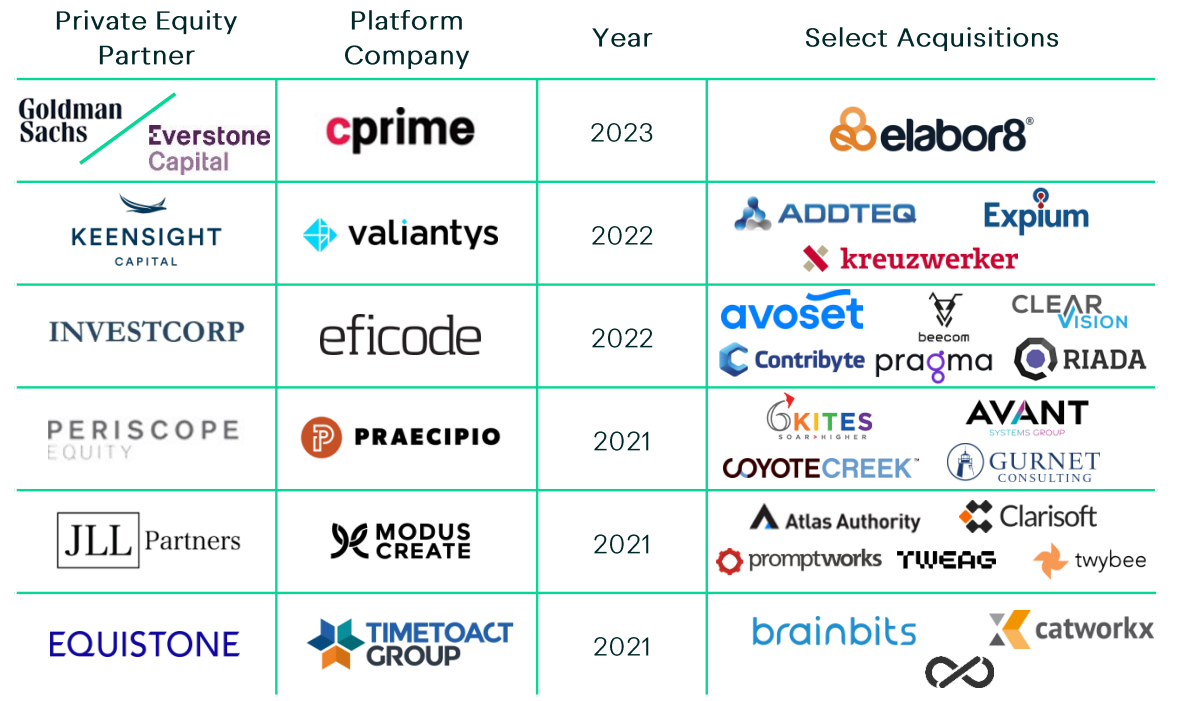

As with any fragmented, lucrative industry it was a matter of time Private Equity spotted the consolidation opportunity:

Source: Q Advisors

Who is Europe’s largest and most acquisitive Atlassian partner rollup?

Two names are neck and neck: TIMETOACT from Germany and Adaptavist from the UK.

TIMETOACT reported 2023 revenue of €320M ($340M). Adaptavist is of a similar size, with with 2024 (September year-end) revenues exceeding £300M (c.$380M). Adaptavist’s revenues in GBP terms have grown more than 70-fold in a decade (see the chart below; in USD terms, approx. 60-fold).

Source: Companies House, RollUpEurope analysis

There is one big difference though.

TIMETOACT is majority PE owned (Equistone) and carries meaningful debt.

Adaptavist has taken zero outside investment.

And has practically zero debt.

And the founder Simon Haighton-Williams (pictured below) owns 95%.

Let me repeat: Adaptavist grew 70X+ (in GBP terms) in less than a decade while remaining independent!

Simon Haighton-Williams. Source: Adaptavist

What’s going on?

Let’s find out!

In this article, we discuss:

How Atlassian built a thriving ecosystem

Deep dive on Adaptavist’s business model and M&A strategy (paid subscribers)

List of all companies acquired by Adaptavist (paid subscribers)

Adaptavist’s value creation levers (paid subscribers)

How Atlassian built a thriving ecosystem

Atlassian distinguishes between 3 types of partners:

Solution partners: firms like Adaptavist and Valiantys

App builders: firms like Appfire and SmartBear

Technology partners: firms like AWS, Slack etc.

Fun fact: there are more people reselling Atlassian products (14,000) than there are working for Atlassian (11,000).

Source: Atlassian FY24 Investor Day

At the 2022 SaaStr Cameron Deatsch revealed fascinating facts about the ecosystem:

Here are my takeaways:

Atlassian’s sprawling web of partners and apps was born out of necessity. At the outset, it lacked the distribution, customisation and maintenance muscle - and thus relied on IT small boutiques to do the legwork

In 2012, Adaptavist created the app marketplace to formalise the cottage industry

We are talking serious money: lifetime app sales recently crossed $4B!

Since the ecosystem had been created by mom & pop shop type operations, it was only a matter of time until someone would attempt to roll them up.

How does Adaptavist make money?

In FY 2023 (the most recent period for which public filings are available) Adaptavist reported the following revenue split:

Plug-in (activation) 26%

Licence resale 61%

Product: 1%

Professional & managed services: 12%

The business is structured in 5 business lines which are aligned with Atlassian’s product offering: Agile, DevOps, IT Service Management, Work Management, and Cloud.

Until now, Adaptavist’s M&A activity has focused on the first 3 buckets. We estimate that since 2014, Adaptavist has closed 16 acquisitions of partner and product (app) businesses, with a strong preference for smaller (6 & 7 figure) targets: