- RollUpEurope

- Posts

- My Super Sweet 16: A peek inside Hg’s software rollup portfolio

My Super Sweet 16: A peek inside Hg’s software rollup portfolio

Bonus: how Hg structures deals, case study of Dext ($360M EV)

Alex Prokofjev

April 12, 2024

The UK headquartered PE firm HgCapital manages $65B AuM across several dozen technology firms, including European enterprise software grandees like Visma, IFS and IRIS.

Hg is, without doubt, one of the world’s pre-eminent mid-market software investors. And when it comes to software rollups, it is admittedly second to none.

Source: HgCapital Trust

Our database counts no fewer than 16 software aggregators in which Hg is currently invested. And that’s excluding buy & build platforms in insurance brokerage, accountancies, services etc.

In this article, we shed light on topics such as:

Composition of Hg’s software rollup portfolio

Investment thesis

Portfolio profitability, valuation and gearing metrics

How Hg structures platform investments: case study of Dext (behind paywall)

How we conducted research

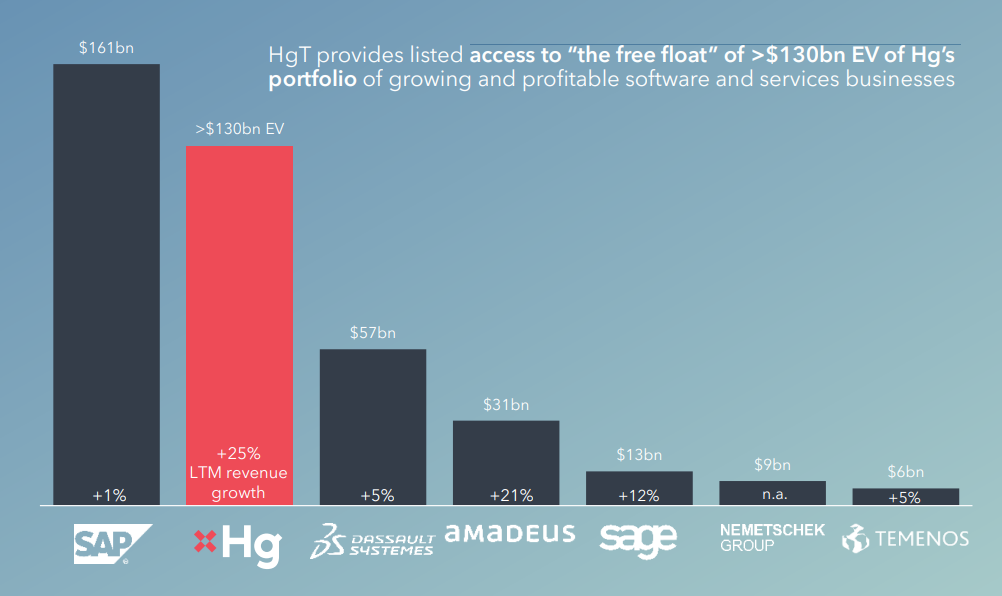

Handily Hg’s largest LP is a publicly listed investment company called HgCapital Trust (HGT).

HGT’s net asset value of £2.3B ($2.9B) translates into an underlying EV of $130B across 50 companies, according to Hg’s calculations. We augmented HGT’s disclosure with public filings and rating agencies’ (Moody’s, S&P) reports.

Hg’s portfolio as a whole is running at a mid teens organic revenue growth and 30%+ EBITDA margins. How do they manage this?

Source: HgCapital Trust

Investment strategy and portfolio composition

From looking at HGT’s portfolio one immediately notices a bias towards tax, accounting, payroll and ERP software. Access, Visma and IFS combined represent 26% of NAV. HGT’s exposure to regulatory compliance software is equally chunky with investments in Litera, Septeo and Ideagen. Combined these industries represent 2/3 of portfolio NAV.

Hg’s acquisition of Azets, a mid-sized UK accounting firm, should come as no surprise given its love for accounting software. Previously, we listed the reasons PE firms are attracted to accountancies and how they structure platform investments (based on the Cooper Parry / Waterland case study).

Here is the full list of the Hg’s 16 software aggregators included in our database:

Name | Industry | Vertical | HQ | Year founded | Major shareholders |

|---|---|---|---|---|---|

Access Group | Enterprise SaaS | ERP | UK | 1991 | TA, Hg |

Benevity | Enterprise SaaS | CSR | Canada | 2008 | Hg |

Bright Software Group | Enterprise SaaS | ERP | Ireland | 2021 | Hg |

Caseware International | Enterprise SaaS | Audit tools | Canada | 1998 | HgCapital |

Citation Group | Enterprise SaaS | Compliance | UK | 1995 | KKR, Hg |

Ideagen | Enterprise SaaS | Compliance | UK | 1993 | Hg |

IFS Workwave | Enterprise SaaS | ERP | Sweden | 1983 | Hg, EQT, TA |

IRIS | Enterprise SaaS | ERP | UK | 1978 | Hg, ICG, Leonard Green |

Litera | Enterprise SaaS | Legaltech | US | 2001 | Hg |

P&I (Personal & Informatik) | Enterprise SaaS | HR | Germany | 1968 | Hg, Permira |

Revalize | Enterprise SaaS | Manufacturing | US | 2021 | Hg, TA |

Sovos | Enterprise SaaS | Tax | US | 1979 | Hg, TA |

Team System | Enterprise SaaS | ERP | Italy | 2013 | Hellman & Friedman, Hg, Silver Lake |

Websites / domains | Hosting | Belgium | 2019 | Hg | |

The Septeo Group | Enterprise SaaS | Legaltech | France | 1998 | Hg |

Visma | Enterprise SaaS | ERP | Norway | 1996 | Hg, Warburg Pincus, TPG, ICG, GA, GIC, CPP |

Size-wise, HGT is invested into very different businesses, ranging from mid-sized ones like Dext (c.$80M revenue) to $1B+ revenue juggernauts like Visma and IFS. The flexibility is due to Hg’s setup across 3 funds. Mercury has the mandate to invest into €100M+ deals. Genesis into €500M+ deals. And Saturn into €1B+ deals.

By and large, Hg is a control investor (60-80%) but by no means the only one. This is one reason why it has been able to hang onto Visma for almost 20 years and still keep a 54.8% stake. We are working on a deep dive into Visma, but for now check out Nick Humphries’ interview on the Business Breakdowns podcast.

Key portfolio metrics

For HGT’s top 20 investments (of which software companies represent majority), 31 December 2023 valuation marks stood at 26.1x EBITDA. What’s more, only 4 out of these 20 companies are valued at <20x EBITDA.

At c.30% EBITDA margin this works out to 8x revenue. The companies were 7.4x levered.

Over-valued?

Over-levered?

Not according to HGT, which sees valuation marks and gearing levels as “consistent with the highly recurring revenues of the businesses that make up the portfolio and is typical for large, high quality software assets in general”.

Indeed, scaled-up ($100M+ revenue) aggregators that comfortably meet Rule 40 on a like for like basis, year after year, are rare and justifiably deserve a premium. However, it is unclear whether these aggregators would achieve similar valuations as listed companies, given the pessimism that prevails in Europe.

How does Hg structure software buyouts?

Let’s take Dext as an example. The digital accounting platform, formerly known as Receipt Bank, was acquired by Hg in April 2021 from several financial investors including Augmentum, Kennet Partners (which reported 4.4x MOIC) and Insight Partners.

Although Dext is not a rollup itself, the transaction provides valuable insight into how experienced PE firms structure software buyouts.

Dext enterprise value was £285M including £5M in deal fees. To put this into context, in 2021 Dext delivered revenue of £36M (i.e. 8x multiple), with 30%+ YoY topline growth and c.90% gross margin.

HGT reported carrying value is 67% above investment cost, which hints at two consecutive years of 30% topline growth.

The said £285M deal value broke down into: