- RollUpEurope

- Posts

- PE firms love Civica - an $800M revenue GovTech juggernaut. So why do they keep passing it around?

PE firms love Civica - an $800M revenue GovTech juggernaut. So why do they keep passing it around?

Double your money in 4 years - or 11x in 16?

Alex Prokofjev

October 17, 2024

Disclaimer: Views expressed here are the author's own and based on public sources. The article is intended for informational purposes only. This is not financial advice. Please consult a professional for investment decisions.

Civica is not exactly a household name. In fact, it is a hidden software champion. If you live in (or do business with) the UK, chances are you have been exposed to Civica's products on multiple occasions.

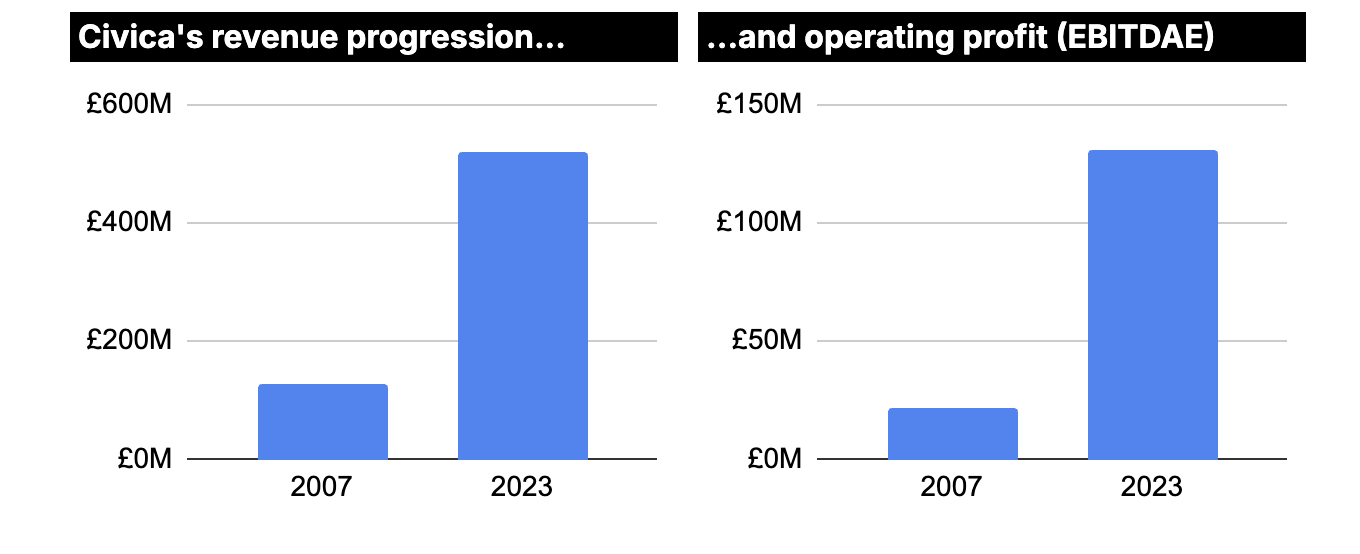

With run-rate revenues approaching £600M ($800M) - of which three-quarters from the UK - Civica's software powers thousands of local authorities, educational institutions and care providers. Civica is what is euphemistically known as a “GovTech rollup”.

Civica is remarkable not only for its discreet ubiquity, but also for the metronomic returns it has delivered to private equity.

Since 2008, Civica has been owned by no fewer than 4 PE firms:

3i took Civica private in 2008

In 2013, 3i exited to OMERS

In turn, OMERS sold Civica to Partners Group in 2017

Finally, in May 2024, Blackstone took over from Partners

During this time, Civica's revenue and operating profits have grown at CAGRs of 9% and 12%, respectively, aided in no small part by M&A.

Source: UK Companies House, Rollupeurope estimates

Realised investor MOICs have ranged 2.1x to 2.6x. This is 4-6 year holding periods. Not terrible, but not spectacular either.