- RollUpEurope

- Posts

- How much dilution is OK? Lessons from 7 aggregators in ecommerce, Youtube and software

How much dilution is OK? Lessons from 7 aggregators in ecommerce, Youtube and software

Founders, leverage this data to get the deal that YOU want!

Alex Prokofjev

July 09, 2024

Got a great rollup idea - but don’t fancy working “just” for carried interest?

I get it. Don’t sell yourself short.

You might be able to raise initial funding the same way that non-acquisitive startups do i.e. while retaining majority.

As we explained in this article, the aggregators that have succeeded in pulling off the trick, have a few things in common:

A distinct investment thesis anchored in a specific vertical, geography - or both

Bargaining power: no dominant capital provider

Ability to fund M&A with relatively little equity

Platform value add (lower churn, cross-sell etc.) with a clear implementation timeline

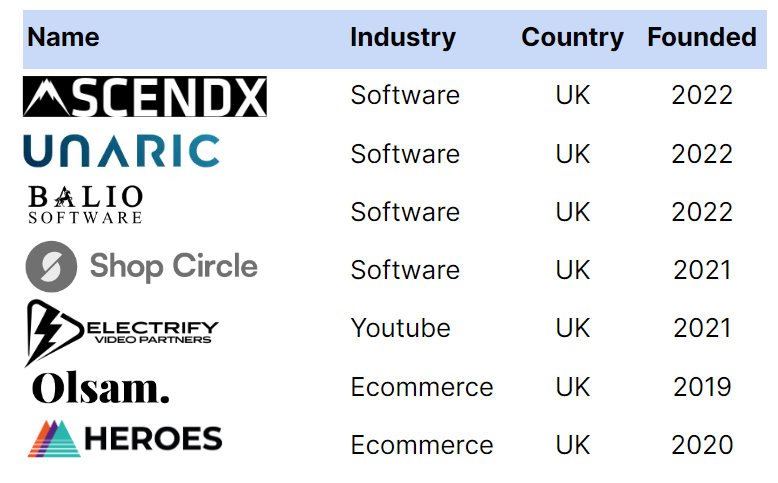

For this article, we reviewed 7 aggregators that have collectively raised nearly $200M in equity and $1B in debt.

All 7 are technology serial acquirers that are <5 years old and are based in the UK. Industry-wise, we are looking at B2B software (4x), Youtube channels (1x) and ecommerce brands (2x).

In this article, we will:

Teach you to recognise (and avoid) parasite intermediaries

Discuss what is and isn’t “market” in VC structure deals

Show how Electrify Video Partners, a Youtube channel rollup, brought in KKR alumni to drive sustained value increase - and what terms they offered to investors. We explain obscure concepts such as “Minimum Return in a Minority Dragged Sale”

Examine the rollercoaster ride of Olsam, an Amazon brand rollup

Before we tuck in. In case you are scratching your head about cover image, I will offer you a clue. Moonbug, the Youtube rollup that owns, inter alia, the Cocomelon nursery rhyme series, was acquired by a Blackstone backed media platform 3 years ago. For a cool $3B.

Source: Moonbug

If you have, or have had a toddler, you will know what I am talking about.

This is serious business. Cocomelon’s Youtube channel has 177M subscribers. My personal favourite, The Wheels on the Bus, has 6 billion views.

How to spot a bad deal

First things first: be prepared to cross institutional investors off your list. Especially Private Equity and search fund investors. They may come in at a later stage, but by default they get the equity and you get the carry.

Family offices and finance and law bigwigs. This is your prime audience.

I shiver a bit as I write these lines. Because if your Rolodex isn’t thick enough, you will find knocking on doors excruciatingly difficult. Unlike with search funds, the market for VC style funding is extremely non-transparent, and borderline hostile to cold outreach.

For now, anyway.

This inaccessibility allows unscrupulous introducers to peddle access in return for astronomic commissions. A typical term sheet might look something like this:

Give up 60% for a $5M equity investment

The investors end up with 25% and the promoter 35% (!)

The promoter will also help you raise debt - if you fancy the high-yield variety

The reason we are so scathing about introducers is because in 90% of all cases they bring very little operational or M&A expertise to the table. Worse, they are disinclined to take risks and would want you to have several million of EBITDA under LOI before disbursing the funds.

Does this sound like a good deal to you?

To me, this sounds like profiteering from desperate founders!

What is “market”, anyway?

Looking at the table below, we can draw several conclusions: