- RollUpEurope

- Posts

- As VMS hype continues, what will be in vogue in 2025?

As VMS hype continues, what will be in vogue in 2025?

Alex Prokofjev

December 17, 2024

Disclaimer: Views expressed here are the author's own and based on public sources. The article is intended for informational purposes only. This is not financial advice. Please consult a professional for investment decisions.

******************

How can you tell that an investment trend is peaking? When every other mid-level PE or growth equity professional tells you they are working on “a niche compounding strategy”!

Yes, I am talking about Vertical Market Software (VMS) rollups.

We are now into the fifth year of an investment boom that has persisted despite vastly increased supply of aggregators and, uhm, the growing threat from AI.

This boom has been great for the aggregators (and their investors) who got going at the right time. Think AppFire’s M&A pivot circa 2019. What about the rest of us? Is it too late to get involved? We don’t think so: provided you know what you are doing.

In this article, we cover 4 topics:

Firstly, we take stock of the “sponsorless” software aggregator landscape: we review the founders’ backgrounds - and their backers’.

Secondly, we “roast” a generic VMS rollup pitch and describe what we believe to be two viable investment strategies: thematic / buy & build and decentralised / HoldCo.

Thirdly, speaking of buy & build: we describe two en vogue sub-strategies: app-store-focused aggregators like Shop Circle and AscendX, and those that focus on the “cloud marketplace” trio of Microsoft Azure, AWS and Google Cloud, like Aries. Stay tuned for a deep dive on Friday!

Fourthly and finally, we make predictions for 2025 and beyond.

Let’s go!

VMS HoldCos are a recent phenomenon

Of the circa 250 software serial acquirers that we track, one-third were established after 2020 (note: full database available to annual subscribers). This includes more than 30 aggregators born in the last 2 years alone. We are talking about names like Azlin, AscendX, Recur, Comet, Ranger and Emergence.

Source: RollUpEurope analysis

Can you guess what they all have in common?

In fact, almost nothing - bar the founders’ backgrounds. These days, the marginal software rollup is the thought product of a mid level investment professional from someplace like Hg Capital or Sapphire (Zoe Zhao and Annalise Dragic / Azlin). Or Accel (Charlie and Henry / Recur). Or TA Associates (Henry Zhang / Emergence). Or TCV (Jessiah Straw / Ranger). Throw in a few investment bankers (think Jarle Mork / Confirma) and sell-side researchers (Luca Cartechini / Shop Circle), and you get the full picture.

Sidenote: Private Equity is much less likely to back someone without operating background for the software rollup CEO position.

Azlin’s founders Zoe and Annalise have investment background - as do Azlin’s investors

What about the investors? Having compiled a list of 350+ investors behind 20+ sponsorless rollups spanning the online and offline realms, the pattern is clear. The investors are not that different from the founders, just a decade or two older (and quite a bit wealthier).

Shop Circle was backed by a number of hedge fund types - the people that Luca had probably met during his time at Jefferies as an analyst of internet stocks. The cap tables of Heroes, the ecommerce rollup now in administration, and Abingdon, a VMS HoldCo, read like the who’s who of the British private equity industry. AscendX has Turkish family offices. The Berlin based Youtube aggregator LunarX teems with Rocket Internet alumni.

Following this path increases your chance of success.

Does your VMS rollup have a North Star?

The dozen or so pitch decks we have seen boil down to these 3 investment highlights:

Vertical Market Software is eating the world

XYZ is where it is at (ServiceNow plugins, manufacturing ERPs etc.)

We will buy steady companies cheaply - and make them better

Better how? Through embedded payments, improved go-to-market, and progressively more vague categories like “product” and “AI implementation”.

Make no mistake: we are not trying to disparage rollups. However, in order to give your aggregator idea a fighting chance, founders have to ask themselves tough questions. Like, what practical experience does my team have with reducing churn and driving cross-sell?

It is not that the VMS rollup thesis is unproven. Quite the opposite.

PE backed, tightly integrated rollups like IDERA and Therapy Brands have been wildly successful because they dominate the markets for diagnostic tools and behavioral health, respectively. Web hosting rollups like team.blue and group.one have aced cross-sell by internalising scores of third party tools through M&A.

Further reading:

On the other end of the spectrum sit decentralised capital allocation beasts like Banyan, Visma and Constellation Software.

Do you know what 1% organic growth plus 30% ROIC, times 30 years, gets you? A C$100B (US$70B) market cap!

Similarly to Constellation, Visma does not integrate. Unlike Constellation, it is known for paying generous multiples (we calculate >4x revenue on average). And yet, time and again, Visma manages to find businesses that grow 15%, 20% for a long time.

The problem is that too many sponsorless rollups try to do both. This is a recipe for disaster.

Pick your North Star, and stay on your path:

Path 1: you integrate well, and cross-sell the resulting product suite into a tightly defined ICP

Path 2: you ace the capital allocation game, with an ultra-thin overhead.

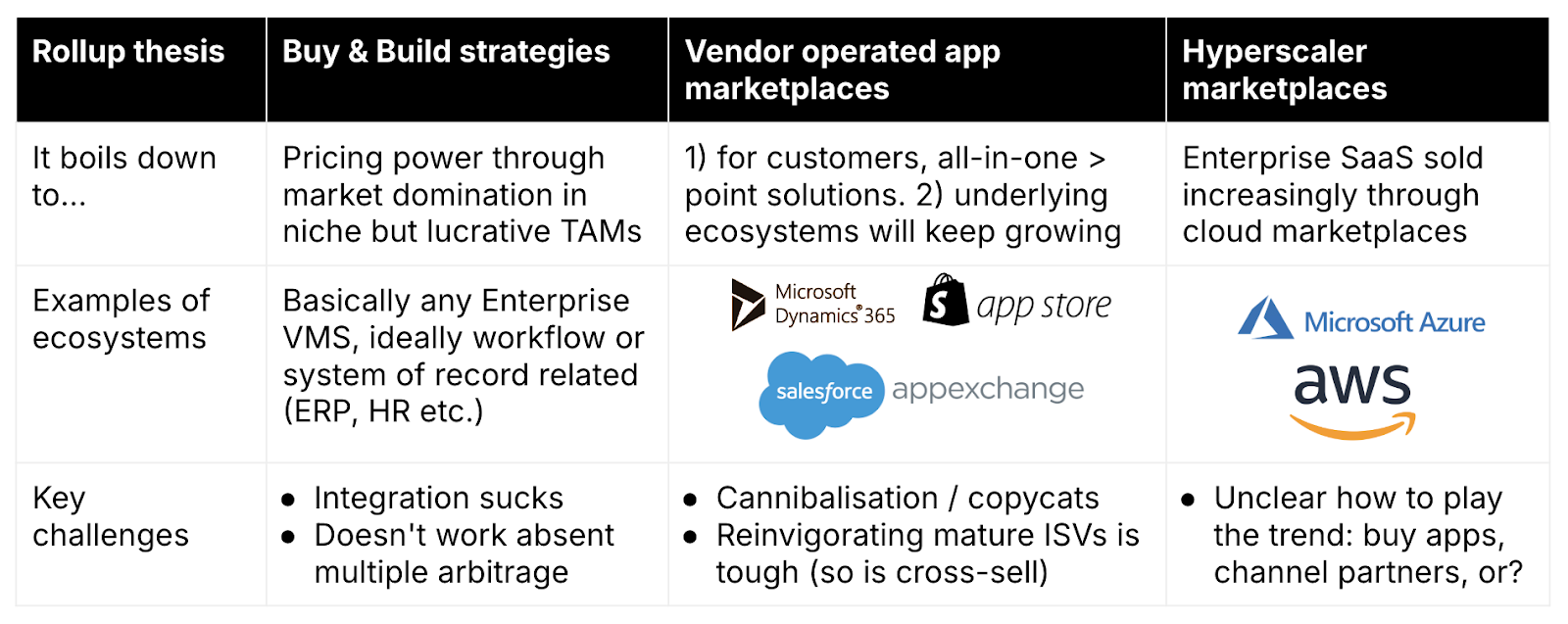

OK, I like thematic strategies…what is on offer?

Let’s say you chose Path 1. What options are available?

We can think of 3:

The good old PE buy & build

Vendor operated app marketplaces

Cloud “hyperscaler” marketplaces

We remain convinced that app marketplaces (see our deep dives on the Salesforce and Shopify/Amazon SaaS aggregator landscapes) offer tremendous potential for consolidation, especially for cybersecurity and data analysis use cases.

We would be cautious with SMB centric, horizontal software like Wix, Canva etc. (basically the creator economy) given the potentially lethal combination of high churn and high risks of cannibalisation / AI disruption.

Source: RollUpEurope analysis

The third strategy, cloud marketplace rollups, is rapidly becoming popular. But what exactly are those “cloud marketplaces”? To quote the market research firm Canalys: