- RollUpEurope

- Posts

- Always Be Rolling? 30 million reasons sellers should roll over equity in PE buy & builds

Always Be Rolling? 30 million reasons sellers should roll over equity in PE buy & builds

The software rollup Totalmobile was sold twice. The founders struck gold twice. Here’s how.

Alex Prokofjev

December 12, 2024

Disclaimer: Views and calculations presented here are the author's own and based on public sources. The article is intended for informational purposes only. This is not financial advice. Please consult a professional for investment decisions.

***

Earlier this year, we ran a series of articles deconstructing spectacular returns achieved by mid market Private Equity investors such as Horizon Capital (4.6x MOIC with Totalmobile) and Literacy Capital (10x with Kernel Global).

However, it is not only GPs and LPs that scored big in both cases. Management too. And, given the rapidly growing share of “pass the parcel” transactions (PE buyer and PE seller), it is not uncommon for the same portfolio company management to cash out 2 or 3 times in the course of a decade, through equity rollovers and top-ups.

Today, using the example of Totalmobile, we will show you how the 5 founders shared an estimated £40M+ ($50M+) windfall over the course of 5 years - and 2 sponsors.

A surprising fact is that almost $30M of that cash came from the rollover: years after the executives had stepped out from the company!

What is Totalmobile?

We highly recommend you check out our Totalmobile case study before embarking on this article. To recap:

Totalmobile is a field service management software vendor from Northern Ireland…

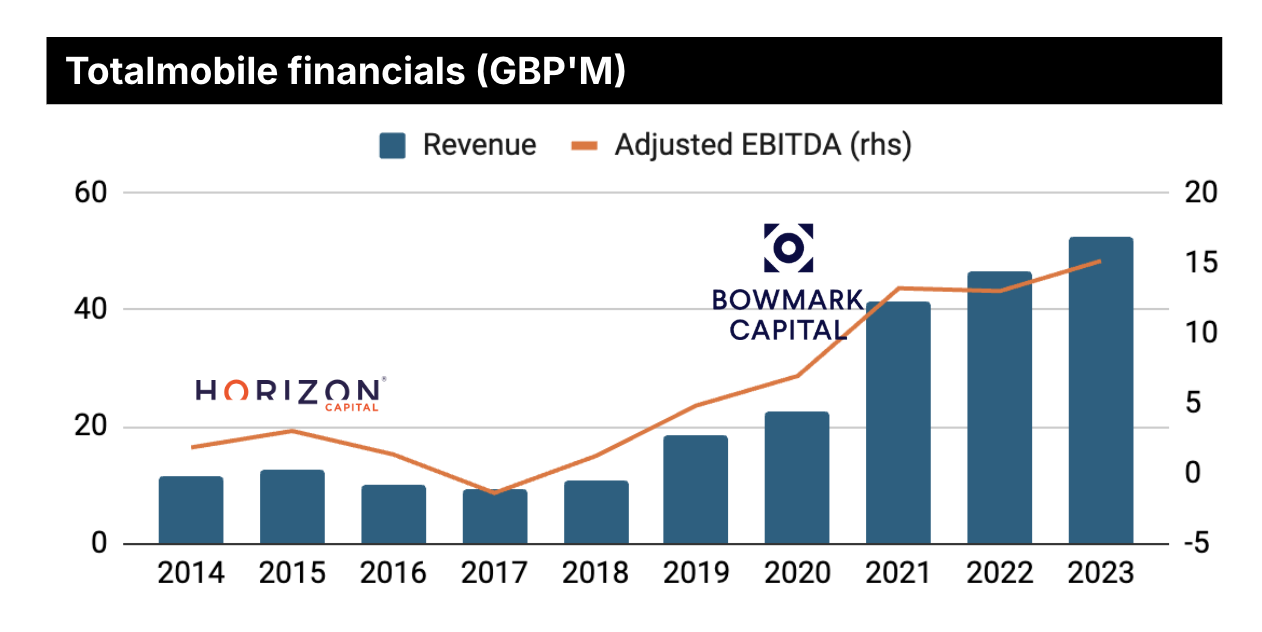

…which has been acquired by PE twice - by Horizon Capital in 2015 and by Bowmark in 2020

In the decade under PE ownership, Totalmobile grew revenue from £10M to £60M+ off the back of add-on M&A and the transition from perpetual licence to SaaS

Source: UK Companies House

Bottom line: back in 2020, Horizon exited Totalmobile to Bowmark for £138M, crystallising a reported 4.6x MOIC and 38% IRR (source).

This solid outcome was far from a walk in the park.

During these 5 years, Totalmobile faced numerous challenges including a drop in revenues, Covid-19 and executive departures. Key to Horizon’s eventual steading of the ship was its proactive cap table management. In plain English, faced with many mouths to feed, Horizon designed an elaborate Management Incentive Plan table that (a) protected the founders’ rollover in a downside case and (b) richly rewarded the retained management team in an upside case.

Below, we explain:

Who got paid, and how much, at the 2015 and the 2020 exits

Downside protection mechanisms used by PE

How Horizon accommodated equity grants to the new leadership without upsetting the founders

Let’s dive in!

A close-up at the original PE exit and the subsequent rollover

As befits a small (£3M / $4M EBITDA), bootstrapped software company, coming up to the 2015 sale Totalmobile sported a straightforward cap table. Colin Reid (CEO), William Surgin (Head of Product) and Ronald Geddis (Head of Sales) combined owned 64%. The dozen or so employees held the remaining 36%.

Colin Reid (Source: Totalmobile)

Horizon paid £25M cash for 100% of Totalmobile, plus an £8M vendor loan. The CEO, the Head of Product and the Head of Sales each collected £5-6M. The CFO and the CTO, £1M+ each.

Not a bad outcome, but not a life-changing one. The best was yet to come.

Horizon financed the buyout through a shareholder loan that sat between external debt and common equity. That common was tranched into 4 classes that ranked pari passu. Horizon owned 61% (all A shares). The management owned 39% - of which the incoming CEO Jim Darragh received 6% and the incoming Chairman David Carman 2%. This equity pot was split into:

B1 and B2 shares - linked to the vendor loan and therefore not subject to good / bad leaver provisions (as befits rollover equity)

C shares - subject to a 5-year vesting schedule with a 1-year cliff

Within two years, the leadership team changed beyond recognition. The Head of Sales was gone. The CEO was gone. The COO was gone. Even the new (!) Chairman was gone. Judging by the fact that all four had their C share grants clawed back, the departures may have not been entirely anticipated and / or amicable.

Sidenote: even “good leavers” would have felt short-changed for the way that “market value” was defined in the Articles of Association of Totalmobile. “Not more than 8 times EBITDA of the Group as set out in the most recently available audited consolidated Group accounts”. In other words, the underlying multiple could be significantly lower than the 8x, once YTD organic growth and recent acquisitions were factored in.

How to reboot a cap table

Old folks out, new folks in. Horizon had to act fast to rebuild the leadership team. In rebooting the Management Incentive Plan, it came up with an ingenious solution: layer 4 additional share classes (D, E, F and G) on top of the existing 4 (A, B1, B2 and C). Each of these share classes served a distinct purpose.